Costs and revenues

· Costs = the expenses a business incurs when operating and producing goods/services.

· Revenue = the income from sales.

· This topic focuses on being able to identify, classify and apply fixed, variable, direct, indirect/overhead costs, plus total revenue and revenue streams.

Cost classifications: fixed and variable

· Fixed costs = costs that do not change in total as output changes in the short run.

· Common examples: rent, insurance, salaried management, loan interest, factory lease.

· Variable costs = costs that change with output. The more units produced/sold, the higher the total variable cost.

· Common examples: raw materials, packaging, piece-rate wages, sales commission, delivery costs per order.

· Exam point: fixed costs stay constant in total, while variable costs rise or fall with output.

· Do not confuse total fixed cost with fixed cost per unit: if output rises, fixed cost per unit falls.

· A cost can be fixed without being direct, and variable without being indirect. These are different ways of classifying costs.

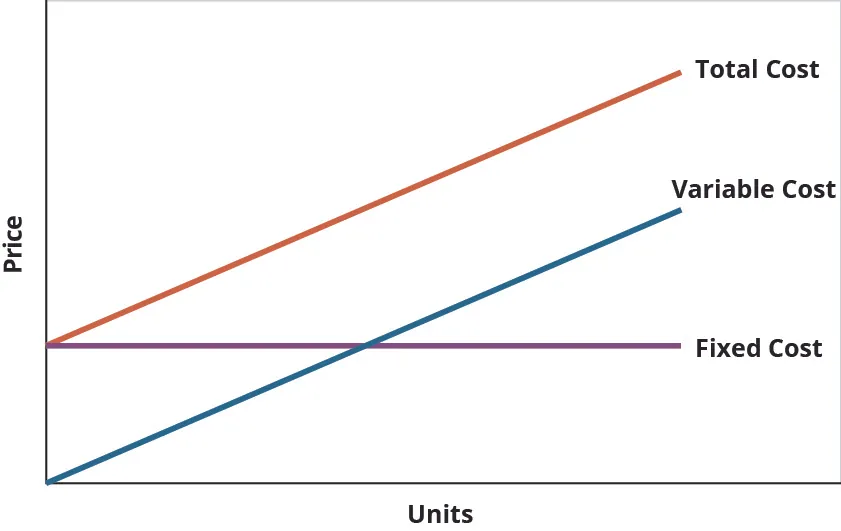

This diagram shows fixed cost as a horizontal line, variable cost rising with output, and total cost starting at the fixed-cost level and rising as output increases. It is useful for explaining why total cost = fixed cost + variable cost. It also helps students visualize why higher output does not change total fixed cost. Source

Cost classifications: direct and indirect/overhead

· Direct costs = costs that can be clearly linked to a specific product, service or cost unit.

· Common examples: wood for a table, fabric for a dress, wages of workers making one product, ingredients for one meal.

· Indirect costs / overheads = costs that cannot be directly traced to one specific unit of output and are shared across the business.

· Common examples: factory rent, electricity, cleaning, administration salaries, security, general advertising.

· Overheads are usually ongoing business costs that support production rather than becoming part of the product itself.

· Exam point: ask, “Can this cost be directly attributed to one product/service?” If yes → direct. If no → indirect/overhead.

· Important link: direct costs are often variable, but not always; indirect costs can be fixed or variable.

This resource helps distinguish direct costs from indirect/overhead costs using business examples. It is useful for exam questions that ask students to classify a cost in context. It also reinforces that indirect costs may be fixed or variable. Source

Total revenue

· Total revenue (TR) = the money received from sales over a period.

· Formula:

· Where P = price per unit and Q = quantity sold.

· Example: if a business sells 500 units at 6,000.

· If price stays the same, selling more units increases total revenue.

· If quantity sold stays the same, raising price increases total revenue.

· In exam questions, always check whether the data gives selling price, quantity sold, or both.

· Do not confuse revenue with profit: profit = revenue − costs.

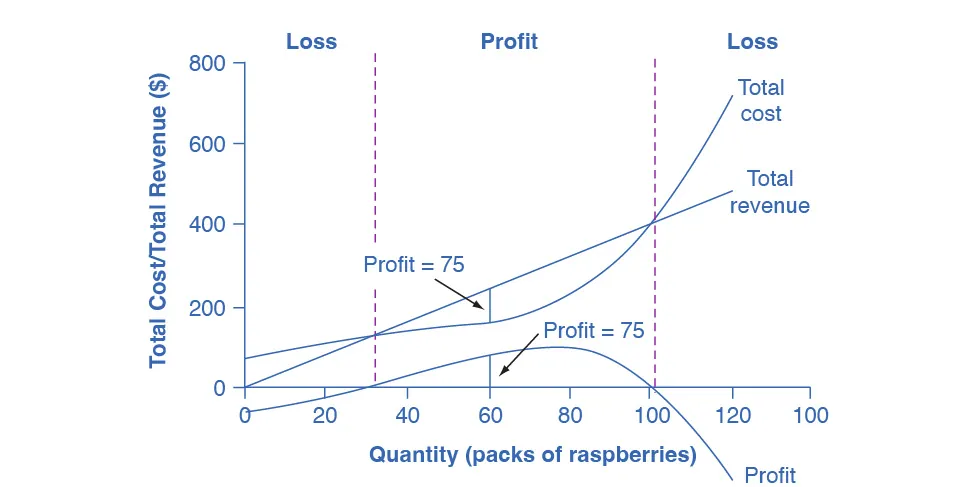

This graph compares total revenue and total cost as output changes. It shows that profit is the gap between the two lines, so it is excellent for avoiding the common mistake of treating revenue as profit. It also shows that total revenue typically rises with quantity sold. Source

Revenue streams

· Revenue streams = the different sources of income a business earns from its activities.

· A business may rely on one main revenue stream or multiple revenue streams.

· Examples: product sales, subscription fees, delivery charges, advertising income, commission, licensing, service/repair fees.

· Example: a gym may earn revenue from memberships, personal training, merchandise sales and class fees.

· Multiple revenue streams can reduce risk because the business is less dependent on one source of income.

· In case studies, identify not just how much revenue is earned, but where it comes from.

Exam application and common traps

· Be ready to classify a cost in context, not just define it.

· A cost may fit two classifications at once: for example, direct materials are usually direct and variable.

· Rent is usually fixed and indirect/overhead.

· Commission is usually variable and may be direct if tied to each sale.

· Total revenue is not the same as cash flow or profit.

· If the question asks for revenue streams, give separate named sources of income, not just the formula for total revenue.

· Use business examples whenever possible because the syllabus explicitly requires costs and revenues using examples.

· Strong exam answers often use a mini-structure: identify → define → apply to the case.

Quick examples you can use in answers

· Bakery: flour = direct variable cost; shop rent = fixed indirect cost.

· Clothing business: fabric = direct variable cost; manager salary = fixed indirect cost.

· Taxi firm: fuel = variable cost; vehicle insurance = fixed cost.

· Streaming platform: subscription fees = key revenue stream; advertising income may be another revenue stream.

· Restaurant: ingredients = direct cost; electricity and cleaning = indirect/overhead costs.

Checklist: can you do this?

· Define fixed, variable, direct and indirect/overhead costs clearly.

· Classify business costs from a case study and justify the classification with a brief reason.

· Calculate total revenue using .

· Identify different revenue streams for a business in context.

· Avoid the exam trap of confusing revenue, profit and cash flow.

Dave is a Cambridge Economics graduate with over 8 years of tutoring expertise in Economics & Business Studies. He crafts resources for A-Level, IB, & GCSE and excels at enhancing students' understanding & confidence in these subjects.

Dave is a Cambridge Economics graduate with over 8 years of tutoring expertise in Economics & Business Studies. He crafts resources for A-Level, IB, & GCSE and excels at enhancing students' understanding & confidence in these subjects.