AQA Specification focus:

‘The economists’ model of wage determination in a perfectly competitive labour market; the role of market forces in determining relative wage rates; appreciate that all real-world markets are imperfectly competitive to a greater or lesser extent.’

Introduction

In a perfectly competitive labour market, wages and employment are determined by interactions of demand and supply, where market forces establish equilibrium wage rates and employment levels.

The Model of Wage Determination in Perfect Competition

In a perfectly competitive labour market, there are many firms hiring workers, many workers offering labour, and neither side has power to set wages unilaterally. Instead, the wage rate is set by the balance of supply and demand.

Perfectly Competitive Labour Market: A labour market structure where numerous employers and workers exist, all are wage-takers, and labour is homogeneous.

Conditions for Perfect Competition in Labour Markets

Large number of employers and workers.

Homogeneous labour — no differentiation in skills or productivity.

Perfect information — both employers and employees are fully aware of wage rates and job opportunities.

Free entry and exit — workers can move freely between jobs without barriers.

Wage-taking behaviour — no individual employer or worker can influence the wage rate.

These assumptions are theoretical and rarely met in reality, but they form the basis for understanding competitive labour market wage determination.

Labour Demand and Market Forces

The demand for labour is a derived demand — it depends on the demand for the goods and services that labour helps produce. Firms hire workers as long as their contribution to revenue exceeds or equals the wage rate.

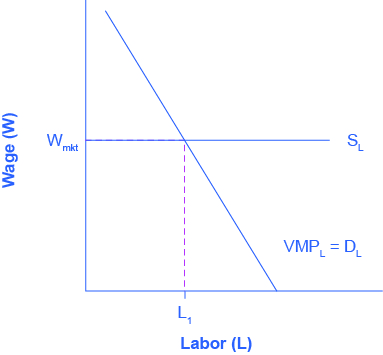

A price-taking firm faces a horizontal labour supply at the market wage. It hires up to the point where the value of the marginal product equals the wage. Source

The Labour Demand Curve

Downward sloping, reflecting the law of diminishing marginal returns — as more workers are hired, each additional worker adds less to output, reducing their marginal revenue product.

Shows the inverse relationship between the wage rate and quantity of labour demanded.

Marginal Revenue Product (MRP): The additional revenue generated by employing one more worker, calculated as marginal product × marginal revenue.

When wage rates fall, firms are willing to employ more workers, and when wage rates rise, fewer workers are employed.

Labour Supply and Market Forces

The supply of labour to a perfectly competitive market depends on the wage rate offered and the willingness of workers to provide their labour.

The Labour Supply Curve

Upward sloping, as higher wages attract more workers into the occupation.

Reflects both monetary incentives (wage levels) and non-monetary considerations (working conditions, job satisfaction, location).

The interaction of labour supply and demand determines the equilibrium wage rate.

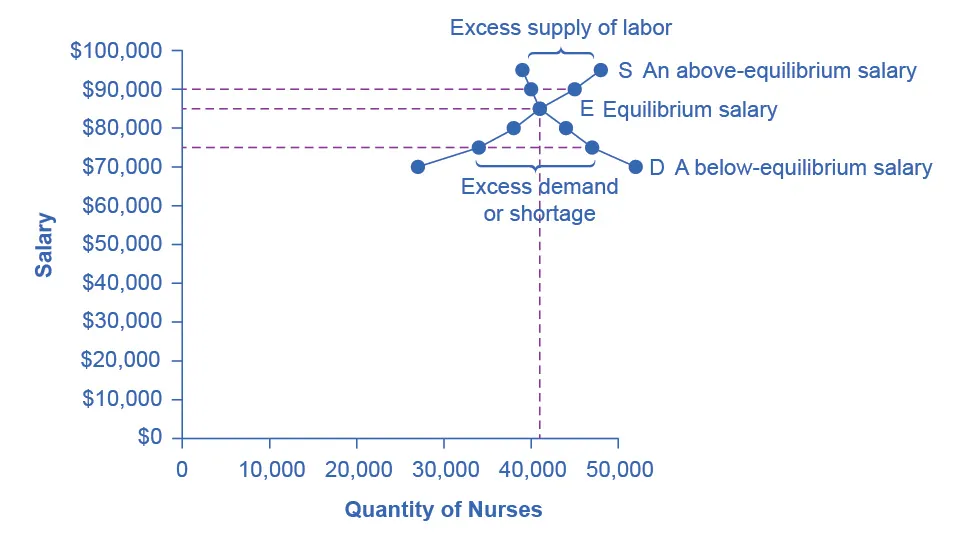

Equilibrium in the labour market occurs where demand for and supply of labour intersect. Above this point there is unemployment; below it, excess demand for labour. Source

Equilibrium Wage Rate and Employment

Determination Process

Intersection point of the demand and supply curves determines the market-clearing wage rate and the number of workers employed.

At this wage:

Firms are willing to hire exactly the number of workers willing to work.

There is no excess supply (unemployment) or excess demand (labour shortage).

Equilibrium Wage Rate: The wage at which the quantity of labour demanded equals the quantity of labour supplied in a market.

Adjustment Mechanism

If wages are set above equilibrium, excess supply occurs (unemployment). Market forces drive wages down.

If wages are set below equilibrium, excess demand occurs (shortages). Market forces push wages up.

This self-correcting mechanism underpins the economists’ model of competitive labour market equilibrium.

Relative Wage Rates Across Occupations

In competitive markets, wage differences between occupations arise due to variations in:

Labour demand: Higher in industries with strong product demand or higher worker productivity.

Labour supply: Lower in occupations requiring long training or offering poor working conditions.

Transfer earnings: The minimum wage a worker requires to remain in a particular job, influenced by opportunities elsewhere.

These differences explain why wages vary across sectors even under the model of perfect competition.

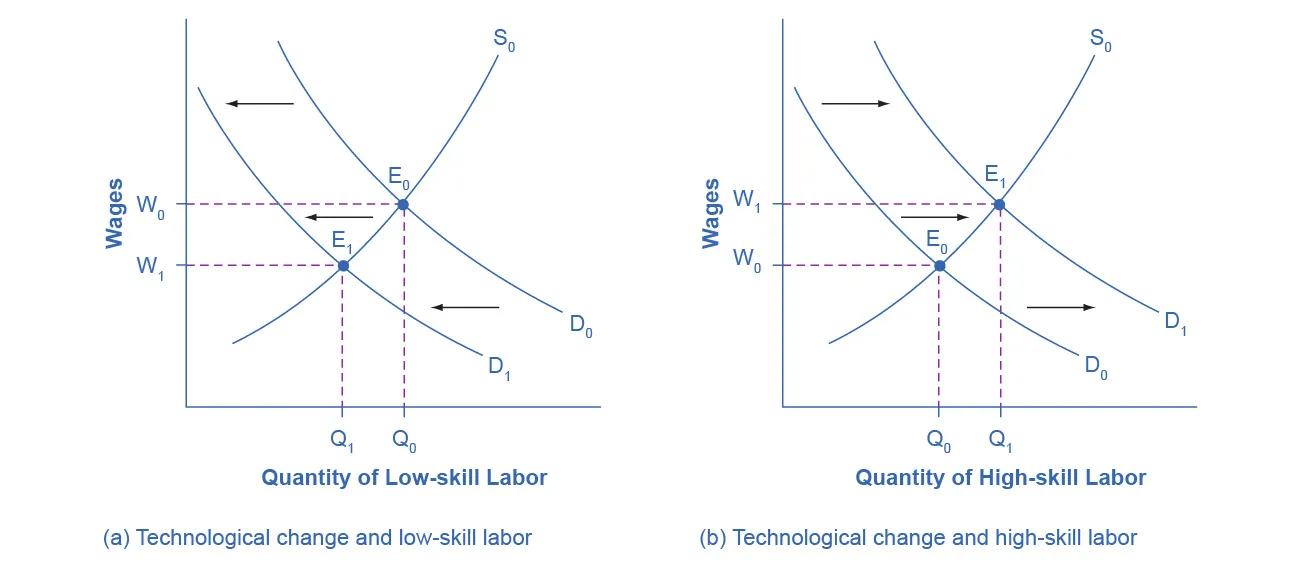

Two labour markets compared: demand shifts down in low-skill work lowering wages, while shifting up in high-skill work raising wages. This explains relative wage differences. Source

Real-World Deviations from Perfect Competition

While the theoretical model provides a benchmark, all real-world labour markets are imperfectly competitive to some degree. Key imperfections include:

Monopsony power — where a single employer dominates hiring.

Trade unions — which can influence wages above equilibrium.

Imperfect information — workers and firms may not know all available opportunities.

Labour immobility — workers face geographical or occupational barriers to moving jobs.

Such imperfections mean that real wages and employment often deviate from the textbook competitive model.

Key Features to Remember

Wage determination in perfectly competitive markets depends entirely on market forces of supply and demand.

Firms and workers are wage-takers — they cannot set wages themselves.

The equilibrium wage rate ensures that labour demand equals labour supply.

Wage differentials between occupations reflect differences in demand and supply conditions.

Real-world markets diverge due to imperfect competition, making the model a theoretical baseline rather than a practical reality.

Practice Questions

Define what is meant by a perfectly competitive labour market. (2 marks)

1 mark for recognising that there are many employers and many workers (no single buyer or seller of labour can influence the wage).

1 mark for stating that firms and workers are wage-takers and that labour is homogeneous/perfect information exists.

Explain how the equilibrium wage rate is determined in a perfectly competitive labour market, using a demand and supply framework. (6 marks)

1 mark for identifying that labour demand is derived from the marginal revenue product of labour.

1 mark for stating that the demand curve for labour is downward sloping.

1 mark for identifying that the supply of labour is upward sloping.

1 mark for stating that the equilibrium wage is set where labour demand equals labour supply.

1 mark for explaining that excess supply (unemployment) or excess demand (labour shortage) occurs when wages are not at equilibrium.

1 mark for clear explanation of how market forces move wages towards equilibrium (self-correcting mechanism).

FAQ

The model assumes perfect information, free mobility of labour, and homogeneous workers. In reality, workers have different skills, moving jobs involves costs, and firms often have more information than employees.

It also assumes no barriers to entry or exit, yet training, qualifications, and location limit labour mobility. This makes the model more of a theoretical benchmark than a real-world description.

Wages reflect the value of the marginal revenue product (MRP) of labour. Firms hire workers up to the point where MRP equals the market wage.

If productivity rises, MRP increases, shifting demand for labour outwards, leading to higher equilibrium wages. Conversely, falling productivity lowers MRP and reduces labour demand.

Wage differences occur due to:

Varying levels of labour demand (higher in industries with strong product demand).

Differences in required training or qualifications.

Non-monetary factors such as risk or working conditions.

These factors shift demand or supply curves in specific occupations, creating distinct equilibrium wages across industries.

The supply curve of labour reflects workers’ opportunity cost of leisure or alternative employment.

As wages rise, the opportunity cost of not working increases, encouraging more people to enter or remain in the labour market. This helps determine the upward slope of the supply curve.

When demand exceeds supply at the current wage, firms compete for workers by offering higher wages.

This encourages additional workers to enter the market and reduces excess demand.

The process continues until a new equilibrium wage and employment level is reached, eliminating the shortage.