AP Syllabus focus: ‘Unexpected inflation redistributes purchasing power between borrowers and lenders.’

Unexpected inflation changes the real value of dollar-denominated payments written into contracts. Because many loans and savings accounts promise fixed nominal repayments, inflation can unexpectedly transfer purchasing power between different groups.

Core idea: inflation changes real (purchasing-power) outcomes

Inflation affects people differently depending on whether their income and payments are fixed in nominal terms or adjust with the price level. The redistribution effect is largest when inflation is unexpected, because contracts were agreed upon using a different anticipated inflation rate.

Unexpected inflation

Unexpected inflation: inflation that is higher or lower than what borrowers, lenders, workers, and firms anticipated when they signed nominal contracts.

When inflation surprises people, the key issue is that the real value of future payments changes after the contract is already set.

Borrowers vs lenders: who gains and who loses?

Most AP Macroeconomics questions focus on credit markets (loans, bonds, mortgages) where repayments are typically fixed in nominal dollars.

If inflation is higher than expected

Borrowers gain: they repay loans with dollars that buy less than expected, so the real burden of debt falls.

Lenders lose: they receive repayments that have lower purchasing power than expected, reducing the real return on saving/lending.

Common borrower “winners” include households with fixed-rate mortgages, firms with long-term fixed-rate debt, and governments that issue long-term nominal bonds. Common lender “losers” include banks, bondholders, and households holding nominal fixed-income assets.

If inflation is lower than expected (or deflation occurs)

Borrowers lose: they repay with dollars that are worth more than expected, so the real burden of debt rises.

Lenders gain: they receive payments with higher purchasing power than expected, increasing the real return.

This is why unexpected disinflation/deflation can be especially stressful for heavily indebted borrowers.

The real interest rate channel (intuition)

A loan’s stated rate is usually a nominal interest rate. What matters for redistribution is the real interest rate, which adjusts for inflation.

When actual inflation differs from expected inflation, the realized real interest rate differs from what both sides thought they agreed to.

Real interest rate

Real interest rate: the inflation-adjusted cost of borrowing (and return to lending), measured in purchasing-power terms.

Even if the nominal interest rate is fixed, the real interest rate changes as inflation changes.

= real interest rate, percent per year

= nominal interest rate, percent per year

= inflation rate, percent per year

If actual inflation rises unexpectedly, falls relative to what was expected, shifting welfare from lenders to borrowers.

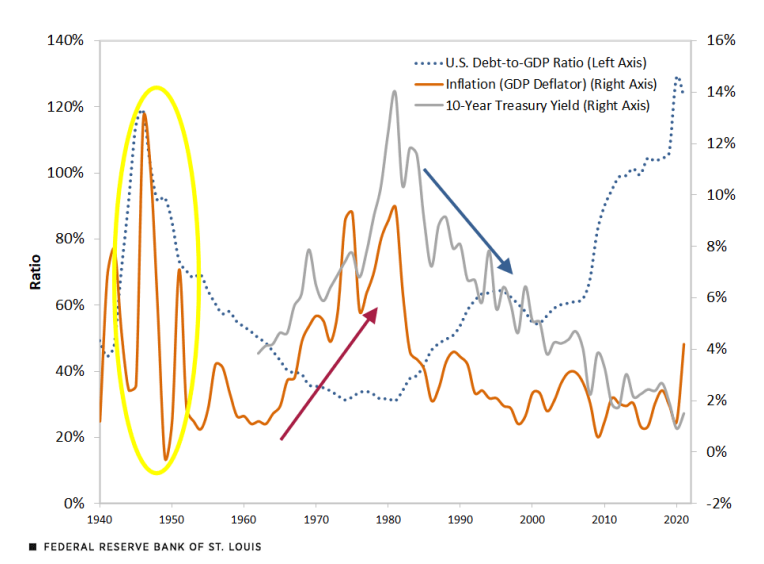

This figure plots inflation (GDP deflator) alongside a long-term nominal interest rate (10-year Treasury yield) and discusses the implied ex-post real yield (nominal yield adjusted for realized inflation). It provides a concrete visual example of how unexpectedly high inflation can drive realized real rates down, which is the channel behind the borrower–lender redistribution effect. Source

If falls unexpectedly, rises, shifting welfare from borrowers to lenders.

Why “expected” inflation is different

Redistribution is not mainly caused by inflation itself, but by inflation surprises. If inflation is fully anticipated:

lenders can charge a higher nominal interest rate to maintain a desired real return

borrowers understand their nominal payments will be in less valuable dollars and accept the terms

many contracts (wages, rents, loans) can be written with built-in adjustments

So, the redistribution effect is strongest when:

debts are long-term

interest rates are fixed

contracts are not indexed to inflation

inflation is volatile and hard to forecast

What AP often tests (how to state it precisely)

When asked about redistribution effects, use clear directional language tied to purchasing power:

“Unexpectedly higher inflation reduces the real value of nominal debts, benefiting borrowers and harming lenders.”

“Unexpectedly lower inflation increases the real value of nominal debts, harming borrowers and benefiting lenders.”

“The effect is a change in the real repayment burden/real return, not the nominal payment amount.”

Practice Questions

(2 marks) State who gains and who loses from higher-than-expected inflation in a fixed-rate loan contract. Briefly explain why.

1 mark: Identifies borrowers gain and lenders lose.

1 mark: Explains that repayments are fixed in nominal terms so higher inflation reduces the real value/purchasing power of repayments (real burden falls).

(5 marks) An economy experiences inflation that is lower than expected after many households take out long-term fixed-rate mortgages. Using the idea of real versus nominal values, explain the redistribution effects between borrowers and lenders.

1 mark: Recognises mortgages are fixed in nominal terms (nominal repayments unchanged).

1 mark: Explains that lower-than-expected inflation raises the purchasing power of money.

1 mark: Concludes borrowers are worse off because the real burden of repayments rises.

1 mark: Concludes lenders are better off because the real value of repayments/real return rises.

1 mark: Uses correct real/nominal terminology consistently (e.g., “real value,” “purchasing power,” “real return”).

FAQ

Indexing ties payments to an inflation measure, so the real value of repayments is stabilised.

Redistribution between borrower and lender is reduced because inflation surprises no longer change purchasing power as much.

Not fully. Variable rates can adjust with inflation expectations and policy rates, but the adjustment may be delayed or incomplete.

Redistribution can still occur during the period before rates reset.

Governments often issue long-term nominal bonds. If inflation rises unexpectedly, tax revenues may rise in nominal terms while the real value of outstanding debt falls.

That shifts purchasing power away from bondholders towards the government.

If pensions/annuities are fixed in nominal terms, higher-than-expected inflation reduces their real income.

This is redistribution from recipients of fixed nominal income to payers of those obligations.

No. Any fixed nominal contract can redistribute: rents, wages, alimony, and long-term supply contracts.

The common mechanism is the unexpected change in purchasing power of predetermined nominal payments.