AP Syllabus focus: ‘Both inflation and deflation impose economic costs on individuals and the broader economy.’

Inflation and deflation change the purchasing power of money and reshape incentives across the economy. Even when anticipated, they can reduce efficiency by distorting price signals, contracts, and spending decisions for households, firms, and governments.

Core ideas and key terms

Inflation vs deflation

Inflation: a sustained increase in the overall price level, meaning each unit of currency buys fewer goods and services.

Inflation matters because many wages, pensions, taxes, and interest payments are written in nominal (dollar) terms, so changing prices can create real effects.

Deflation: a sustained decrease in the overall price level, meaning each unit of currency buys more goods and services.

Deflation is not simply “good because prices are lower”; it can change expectations and increase real burdens in ways that reduce output and employment.

Real interest rates and incentives

= inflation-adjusted borrowing cost (percentage per year)

= stated interest rate in contracts (percentage per year)

= expected rate of inflation (percentage per year)

When expected inflation falls (or becomes negative), the real interest rate tends to rise for a given nominal rate, discouraging borrowing and spending.

Economic costs of inflation

Efficiency and planning costs

Uncertainty about future prices can make long-term planning harder for businesses (pricing, hiring, investment) and households (saving, mortgages).

Menu costs: firms spend resources changing posted prices, updating systems, and renegotiating contracts.

Shoe-leather costs: when inflation is high, people and firms devote time/resources to cash management to avoid holding money that is losing value.

Distorted signals and misallocation

Inflation can blur whether a price increase reflects higher relative demand for a product or just a higher overall price level, leading to weaker price signals and potential misallocation of resources.

If inflation varies across sectors unpredictably, comparing profitability across projects becomes more difficult, potentially reducing productive investment.

Interaction with fixed nominal rules

Where taxes or benefits adjust imperfectly, inflation can change real outcomes (for example, pushing some households into higher brackets without higher real income), increasing perceived unfairness and reducing efficiency.

Economic costs of deflation

Higher real debt burdens and financial stress

With falling prices, fixed nominal debts (mortgages, business loans) become larger in real terms, increasing defaults and bankruptcies.

Financial institutions may tighten lending standards after losses, reducing credit availability and amplifying downturns.

Delayed spending and weaker aggregate demand

If consumers and firms expect prices to keep falling, they may postpone purchases and investment, reducing current spending.

Lower spending can reduce firms’ revenues, leading to layoffs and further reductions in spending (a negative feedback loop).

Downward nominal rigidity and unemployment

Wages are often “sticky” downward in nominal terms due to contracts, morale, and minimum wages.

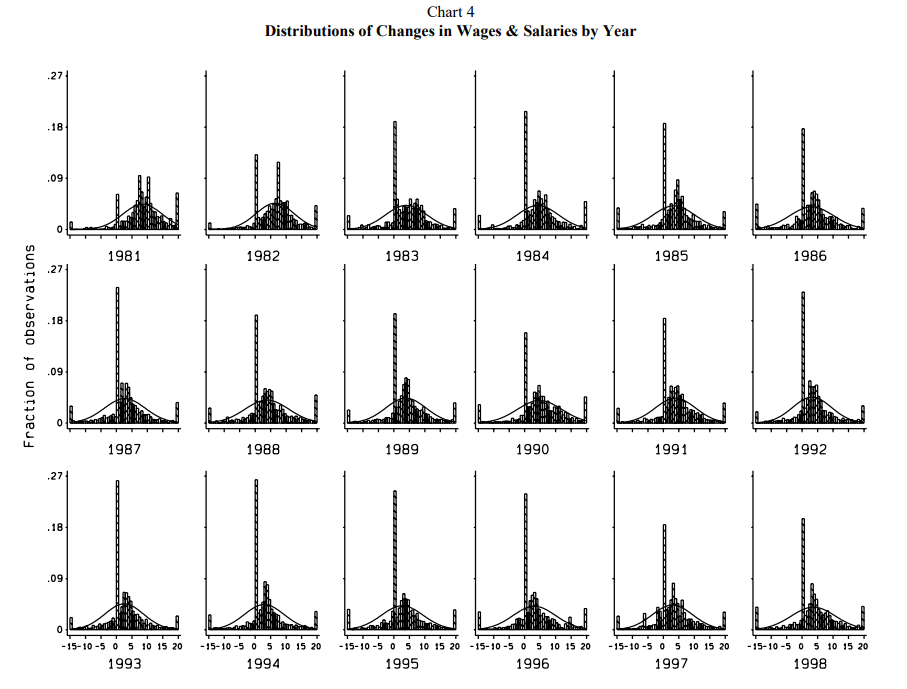

Histogram panels show the distribution of year-to-year nominal wage-and-salary changes, with a prominent spike at 0% (wage freezes) and relatively thin mass below 0% (wage cuts). This clustering illustrates downward nominal wage rigidity: employers adjust labor costs more through reduced hiring/layoffs than through cutting nominal pay, which is especially problematic when deflation raises real wages. Source

With deflation, even unchanged nominal wages can become higher in real terms, raising real labour costs and causing firms to cut employment.

Policy constraints

Deflation increases real interest rates when nominal rates cannot fall much further, limiting the effectiveness of monetary policy and making recoveries harder.

Practice Questions

(2 marks) State two economic costs that can arise during deflation.

1 mark for each valid cost stated, e.g. higher real debt burden, postponed consumption/investment, rising real wages due to stickiness causing unemployment, higher real interest rates.

(6 marks) Explain how deflation can reduce real GDP through its effects on spending and employment.

1 mark: deflation raises the real value of nominal debt.

1 mark: higher real debt increases defaults/financial stress or reduces borrowing.

1 mark: households/firms cut consumption/investment spending.

1 mark: lower spending reduces firms’ revenues/output.

1 mark: firms reduce labour demand/lay off workers.

1 mark: lower income further reduces spending (negative multiplier-style feedback).

FAQ

Mild, stable inflation can be less disruptive than deflation because it reduces the risk of rising real debt burdens and can allow real wages to adjust without nominal wage cuts.

If people expect future prices to be lower, waiting becomes more attractive.

This can depress current consumption and investment even if incomes have not yet fallen.

Deflation increases the real value of money and fixed nominal assets.

But it raises the real burden of fixed nominal debts, so borrowers and leveraged firms can be hit hard through higher real repayments.

Deflation raises real wages even when nominal wages are unchanged.

If firms cannot cut nominal wages, they may instead cut hours or jobs to reduce labour costs.

Because what matters for decisions is the real rate $r \approx i - \pi^e$.

If $\pi^e$ becomes negative, $r$ can rise even when $i$ is low, discouraging borrowing and spending.