The Accounting System

· Accounting system = the organised process used to record, classify, summarise and report business transactions.

· CIE focus: systematic recording, double entry, manual and computerised systems, and accounting concepts underpinning financial accounting.

· Main purpose: produce reliable financial information for decision-making.

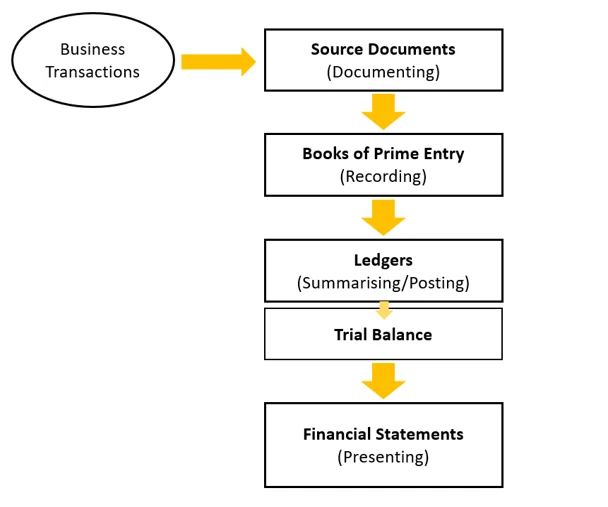

· Every transaction should be supported by source documents, recorded in books of prime entry, posted to ledger accounts, checked through a trial balance, then used to prepare financial statements.

This diagram shows how accounting information flows from business transactions to financial statements. It is useful for understanding the sequence of recording before preparing final accounts. Source

Double Entry System

· Double entry system = every transaction has two equal and opposite effects: one debit and one credit.

· Rule: total debits = total credits for every transaction and for the accounting records overall.

· Debit does not always mean “increase” and credit does not always mean “decrease”; the effect depends on the type of account.

· Basic exam rule:

· Assets increase with a debit and decrease with a credit.

· Expenses increase with a debit and decrease with a credit.

· Liabilities, capital/equity and income/revenue increase with a credit and decrease with a debit.

· Double entry helps maintain the accounting equation and supports accurate ledger records.

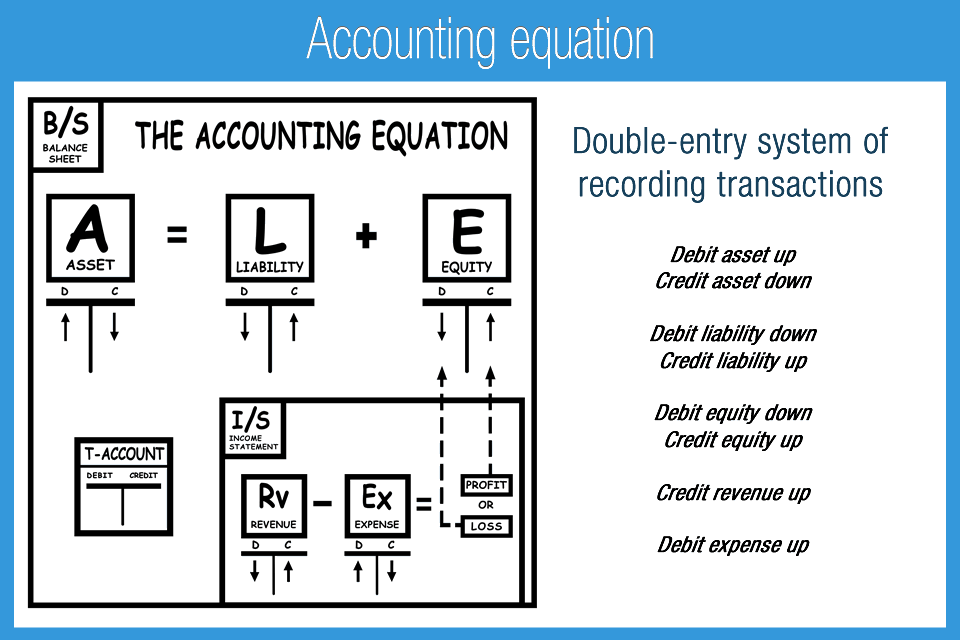

This image links the accounting equation with debit and credit rules. It helps students remember which account types increase on the debit side and which increase on the credit side. Source

Accounting Equation

· Core equation: Assets = Liabilities + Capital/Equity.

· Expanded idea: Capital increases with profit and decreases with drawings or losses.

· Every transaction must keep the equation balanced.

· Examples:

· Owner introduces cash: Assets increase, Capital increases.

· Buy equipment for cash: one asset increases, another asset decreases.

· Buy goods on credit: Assets increase, Liabilities increase.

· The accounting equation is the foundation of double entry bookkeeping.

Books of Prime Entry

· Books of prime entry = first place where transactions are recorded before posting to ledgers.

· They reduce clutter in the ledger and group similar transactions together.

· Main books required by the syllabus:

· Sales journal: credit sales.

· Sales returns journal: goods returned by credit customers.

· Purchases journal: credit purchases.

· Purchases returns journal: goods returned to credit suppliers.

· Cash book: cash and bank receipts/payments; may include discounts.

· General journal: unusual entries, corrections, opening entries, year-end adjustments and non-cash transactions.

· Exam tip: know the source document, book of prime entry, and ledger accounts affected.

Ledger Accounts

· Ledger account = account where transactions are classified and summarised by type.

· Common ledgers include sales ledger, purchases ledger and general/nominal ledger.

· Ledger accounts are often shown as T-accounts with:

· Debit side on the left.

· Credit side on the right.

· Balance carried down (balance c/d) at the end of a period.

· Balance brought down (balance b/d) at the start of the next period.

· Posting from books of prime entry must follow the double entry rules.

· Exam skill: identify the correct accounts, decide debit or credit, and balance the account correctly.

Trial Balance

· Trial balance = list of ledger account balances at a particular date.

· Purpose: check the arithmetical accuracy of the double entry system.

· If total debit balances = total credit balances, the trial balance agrees.

· A trial balance helps locate some errors but does not prove all entries are correct.

· It may not reveal errors such as complete omission, commission, principle, original entry, reversal or compensating errors.

· It is used as a starting point for preparing financial statements.

Full Accounting Records

· Full accounting records mean all transactions are recorded using proper double entry and supporting documents.

· Advantages:

· Provides accurate financial statements.

· Helps owners/managers make informed decisions.

· Supports control, audit trail and error detection.

· Makes it easier to calculate profit, assets, liabilities and capital.

· Disadvantages:

· Can be time-consuming.

· May require trained staff.

· Can be costly for small businesses.

· Errors may still occur if information is entered incorrectly.

Accounting Concepts

· Business entity: business records are kept separate from the owner’s personal affairs.

· Historic cost: assets are usually recorded at original cost.

· Money measurement: only items measurable in money are recorded.

· Going concern: accounts assume the business will continue operating for the foreseeable future.

· Consistency: accounting methods should be applied consistently between periods.

· Prudence: do not overstate assets/profits; provide for expected losses.

· Realisation: revenue is recognised when earned, not necessarily when cash is received.

· Duality: every transaction has two effects, supporting double entry.

· Materiality: only information significant enough to affect decisions must be treated carefully.

· Objectivity: accounting records should be based on verifiable evidence.

· Matching/accruals: income and expenses are matched to the period they relate to.

· Substance over form: record the economic reality, not just the legal form.

Computerised Accounting Systems

· Computerised accounting system = software-based system used to record and process financial transactions.

· Uses include:

· Recording sales, purchases, cash, bank and journal entries.

· Posting automatically to ledger accounts.

· Producing trial balances and financial reports.

· Advantages:

· Faster processing of transactions.

· Improved accuracy if data is entered correctly.

· Easy production of reports and account balances.

· Better storage and retrieval of accounting records.

· Disadvantages:

· Initial purchase/setup cost.

· Need for staff training.

· Risk of data loss, hacking or unauthorised access.

· Over-reliance on software can hide errors if controls are weak.

· CIE note: knowledge of specific accounting software applications is not required.

Data Security in Computerised Accounting

· Use passwords and different access levels for staff.

· Make regular backups and store copies securely.

· Use anti-virus software and security updates.

· Keep an audit trail of changes to records.

· Use authorisation controls for sensitive transactions.

· Protect data from loss, theft, unauthorised changes and cyberattacks.

Exam Decision-Making Focus

· Be ready to evaluate information and recommend suitable accounting actions.

· Link decisions to:

· Accuracy of records.

· Cost of maintaining the system.

· Control and security.

· Reliability of financial information.

· Usefulness for decision-making.

· Strong answers explain both benefits and limitations, then make a justified conclusion.

Checklist: can you do this?

· Explain and apply the double entry system using correct debit and credit entries.

· Use the accounting equation to show the effect of transactions.

· Identify the correct book of prime entry and prepare/post to ledger accounts.

· Explain the purpose and limitations of a trial balance.

· Evaluate manual vs computerised accounting systems, including data security.