Non-current Assets

· Non-current assets = assets used in the business for the longer term, not bought mainly for resale.

· Examples: premises, machinery, motor vehicles, equipment, fixtures and fittings.

· They are shown in the statement of financial position at carrying amount / net book value.

· Carrying amount / NBV = cost or valuation – accumulated depreciation.

· Key exam idea: non-current assets help generate revenue over several accounting periods, so their cost must be spread using depreciation.

Capital and Revenue Expenditure

· Capital expenditure = spending to buy, improve, or extend the useful life of a non-current asset.

· Capital expenditure is recorded as a non-current asset in the statement of financial position.

· Examples: purchase of machinery, delivery and installation costs, legal fees on property purchase, major improvement to equipment.

· Revenue expenditure = day-to-day spending needed to run the business or maintain assets.

· Revenue expenditure is recorded as an expense in the statement of profit or loss.

· Examples: repairs, servicing, fuel, insurance, cleaning, routine maintenance.

· Exam clue: if spending increases earning capacity, extends useful life, or improves asset performance, it is usually capital expenditure.

· If spending only maintains existing condition, it is usually revenue expenditure.

Capital and Revenue Income

· Capital income = income from non-trading or long-term capital sources.

· Examples: proceeds from sale of non-current assets, capital introduced by owner, loan received.

· Revenue income = income earned from normal trading activities.

· Examples: sales revenue, fees received, commission received, rent received.

· Exam focus: classify income correctly because it affects profit calculation and financial statement presentation.

Effects of Incorrect Treatment

· If capital expenditure is treated as revenue expenditure:

· Expenses overstated.

· Profit understated.

· Non-current assets understated.

· Capital employed understated.

· If revenue expenditure is treated as capital expenditure:

· Expenses understated.

· Profit overstated.

· Non-current assets overstated.

· Future depreciation may also be overstated.

· Exam technique: always state the effect on both profit/loss and asset value.

Depreciation: Meaning and Purpose

· Depreciation = the systematic allocation of the depreciable amount of a non-current asset over its useful life.

· It is not the same as setting aside cash to replace the asset.

· It is an expense charged to the statement of profit or loss.

· It reduces the asset’s carrying amount in the statement of financial position.

· Depreciation applies the matching / accruals concept because the cost of using the asset is matched against the revenue it helps generate.

· Depreciation also applies the prudence concept because assets should not be overstated.

· Common causes of depreciation: wear and tear, passage of time, obsolescence, depletion, and technological change.

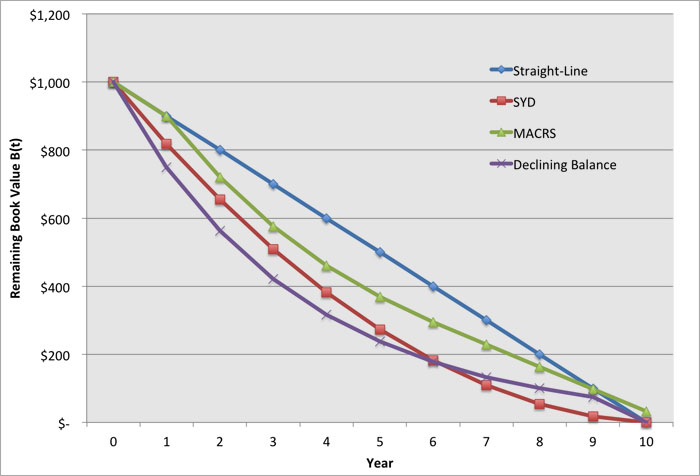

The graph shows how different depreciation methods reduce the book value of an asset over time. It is useful for comparing the constant reduction under straight-line depreciation with the faster early reduction under declining balance methods. Source

Straight-line Method

· Straight-line depreciation charges the same amount of depreciation each year.

· Formula: Annual depreciation = (cost – residual value) ÷ useful life.

· Use when the asset provides equal benefit each year.

· Common for assets such as buildings, fixtures, and office equipment.

· Advantage: simple, consistent, easy to apply.

· Limitation: may be unrealistic if the asset loses more value or provides more benefit in early years.

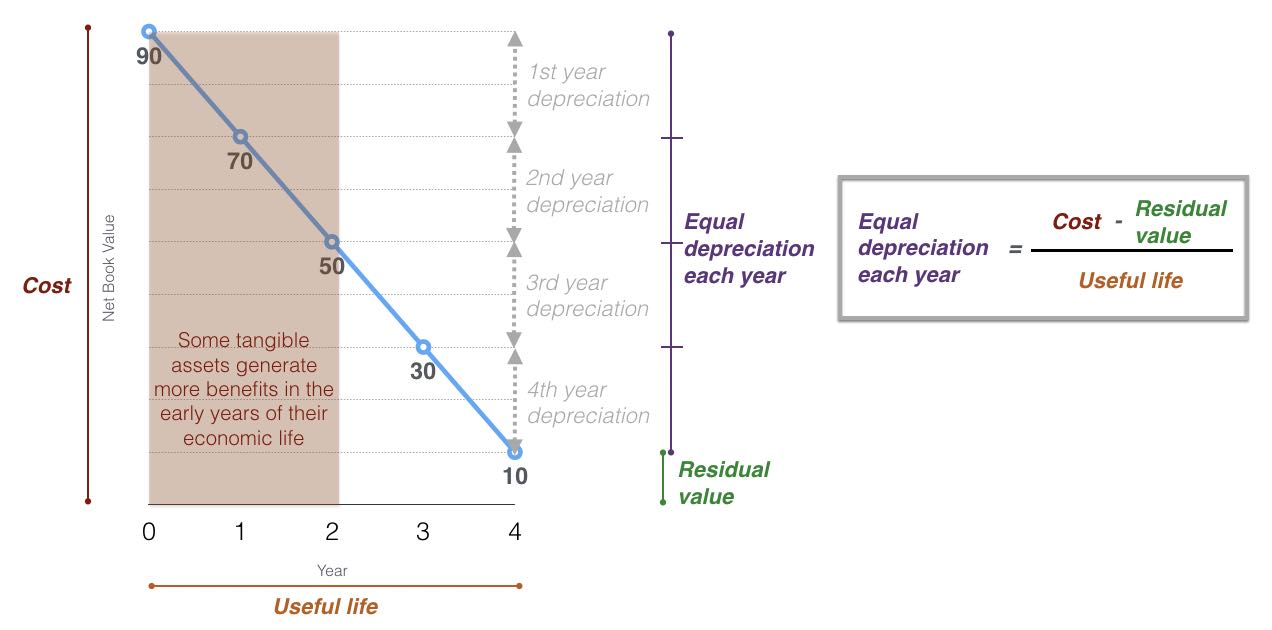

This diagram illustrates straight-line depreciation, where the asset’s net book value falls by an equal amount each year. It clearly shows cost, useful life, annual depreciation, and residual value. Source

Reducing Balance Method

· Reducing balance depreciation charges a fixed percentage on the asset’s carrying amount / NBV each year.

· Formula: Depreciation = carrying amount at start of year × depreciation rate.

· Depreciation is higher in earlier years and lower in later years.

· Use when an asset gives greater benefit in earlier years or loses value quickly.

· Common for assets such as motor vehicles, technology, and machinery.

· Exam warning: depreciation is calculated on reducing book value, not original cost each year.

Choosing the Most Appropriate Depreciation Method

· Choose straight-line when the asset is expected to provide even benefits over its useful life.

· Choose reducing balance when the asset is expected to provide higher benefits in early years.

· The method should follow the consistency concept, so the same method is normally used from year to year.

· The method should give a fair representation of how the asset’s economic benefits are consumed.

· In exam answers, justify the method using the type of asset and the pattern of use.

Cost Model and Revaluation Model

· Cost model: asset is shown at cost less accumulated depreciation.

· Revaluation model: asset is shown at a revalued amount, then depreciated from the revalued figure.

· A revaluation increase usually creates or increases a revaluation reserve.

· A revaluation decrease may reduce any existing revaluation reserve for that asset or be treated as an expense if no reserve exists.

· Revaluation is common for assets such as land and buildings, where market value may change significantly.

· Exam focus: know how revaluation affects asset value, depreciation, and reserves.

Ledger Accounts and Journal Entries

· To record purchase of a non-current asset:

· Dr Non-current asset account

· Cr Bank / Payables / Loan account

· To record annual depreciation:

· Dr Depreciation expense

· Cr Provision for depreciation / Accumulated depreciation

· To record revaluation increase:

· Dr Non-current asset account

· Cr Revaluation reserve

· To record revaluation decrease with no existing reserve:

· Dr Revaluation loss / expense

· Cr Non-current asset account

· Exam tip: use dates, narratives, and correct debit/credit direction in ledger accounts.

Disposal of Non-current Assets

· A disposal account is used to calculate the profit or loss on disposal.

· Step 1: transfer original cost:

· Dr Disposal account

· Cr Non-current asset account

· Step 2: transfer accumulated depreciation:

· Dr Provision for depreciation account

· Cr Disposal account

· Step 3: record sale proceeds:

· Dr Bank / Receivables

· Cr Disposal account

· Step 4: calculate result:

· If disposal account credit side is greater: profit on disposal.

· If disposal account debit side is greater: loss on disposal.

· Formula: Profit/loss on disposal = proceeds – carrying amount at disposal date.

· Carrying amount = cost – accumulated depreciation.

Part Exchange

· Part exchange occurs when an old asset is traded in as part payment for a new asset.

· The trade-in value is treated as the disposal proceeds of the old asset.

· The new asset is recorded at its full purchase price, not only the cash paid.

· Journal logic:

· Dr New non-current asset with full cost.

· Cr Disposal account with trade-in value.

· Cr Bank / Payables with cash balance paid.

· Exam warning: do not confuse trade-in value with cash paid.

Depreciation in Financial Statements

· In the statement of profit or loss, depreciation is shown as an expense.

· Depreciation reduces profit for the year.

· In the statement of financial position, non-current assets are shown at carrying amount / NBV.

· Layout: cost or valuation – accumulated depreciation = carrying amount.

· Depreciation does not directly reduce cash.

· Depreciation affects profit, asset value, and capital employed.

Common Exam Mistakes

· Confusing capital expenditure with revenue expenditure.

· Calculating reducing balance depreciation on cost instead of NBV.

· Forgetting to charge depreciation in the year of disposal if required by the question.

· Treating depreciation as a cash payment.

· Recording a new part-exchange asset at only the cash paid instead of full cost.

· Reversing the disposal entries for cost and accumulated depreciation.

· Forgetting that incorrect classification affects both profit and asset value.

Checklist: can you do this?

· Distinguish capital expenditure, revenue expenditure, capital income, and revenue income.

· Explain how incorrect treatment affects profit/loss and asset value.

· Calculate depreciation using straight-line and reducing balance methods.

· Prepare ledger and journal entries for asset acquisition, depreciation, revaluation, disposal, and part exchange.

· Calculate profit or loss on disposal and show depreciation correctly in the financial statements.