Preparation of Financial Statements

· Purpose: prepare a complete set of financial statements after adjusting the trial balance using the matching/accruals concept and other accounting concepts.

· This topic covers the different formats needed for sole traders, partnerships and limited companies.

· Exam focus: calculate adjustments, prepare statements, explain treatments, and evaluate financial information for business decisions.

Adjustments to draft financial statements

· Accruals: expenses or income relating to the current period but not yet paid/received; adjust to match the correct accounting period.

· Prepayments: expenses or income paid/received in advance; remove the part relating to the next period.

· Irrecoverable debts: remove debts unlikely to be collected; reduces trade receivables and increases expense.

· Irrecoverable debts recovered: cash received from a debt previously written off; record as income.

· Allowance for irrecoverable debts: estimate of future bad debts; reduces trade receivables in the statement of financial position.

· Depreciation: spreads the cost of a non-current asset over its useful life; expense in profit or loss, accumulated depreciation deducted from asset value.

· Inventory valuation: closing inventory affects both cost of sales and current assets.

· Correction of errors: adjust accounts so final statements show accurate profit and financial position.

· Candidates must know how to calculate, record, and show the effect on financial statements for these adjustments.

Sole traders

· Prepare a statement of profit or loss and statement of financial position for a sole trader.

· Questions may use full accounting records or incomplete accounting records.

· The business may be a trading business or a service business.

· Statement of profit or loss: calculate gross profit and profit for the year.

· Trading business: usually includes revenue, opening inventory, purchases, closing inventory, cost of sales, and gross profit.

· Service business: usually no inventory or cost of sales section; focus on income less expenses.

· Statement of financial position: list non-current assets, current assets, current liabilities, and capital.

· Sole trader capital usually follows: opening capital + profit + additional capital − drawings = closing capital.

Partnerships

· Prepare a statement of profit or loss, appropriation account, and statement of financial position for a partnership.

· Questions may use full accounting records or incomplete accounting records, and the business may be trading or service.

· Statement of profit or loss: calculate profit before sharing between partners.

· Appropriation account: shows how profit or loss is divided between partners.

· Common appropriation items: partners’ salaries, interest on capital, interest on drawings, and share of residual profit/loss.

· Capital accounts: record long-term capital invested by each partner.

· Current accounts: record short-term movements such as salary, interest, drawings and profit share.

· Separate capital accounts and current accounts help keep fixed capital separate from yearly profit-sharing adjustments.

· Candidates must know how to prepare partners’ capital and current accounts.

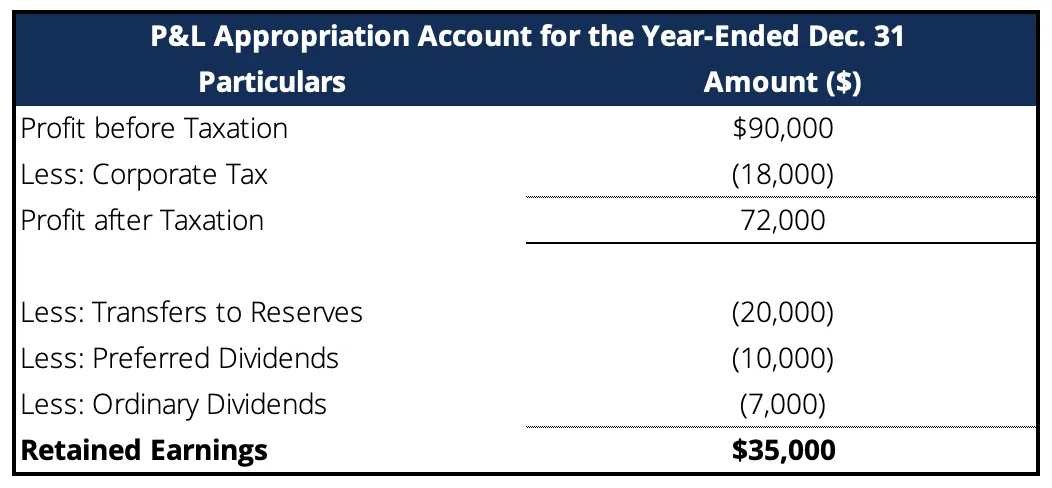

This table shows how partnership profit is appropriated between partners. It demonstrates interest on capital, partners’ salaries, and the residual profit-sharing ratio. Source

Partnership agreement and Partnership Act 1890

· A partnership agreement sets out rules for profit sharing and partner entitlements.

· Typical contents: profit-sharing ratio, partners’ salaries, interest on capital, interest on drawings, interest on partners’ loans, and arrangements for capital.

· Advantages of a partnership agreement: reduces disputes, gives clarity, supports fair treatment of partners.

· Disadvantages: may be time-consuming to prepare and may reduce flexibility if circumstances change.

· If no agreement exists, apply the Partnership Act 1890 rules required by the syllabus.

· Key default rules often tested: no partners’ salaries, profits/losses shared equally, no interest on capital, no interest on drawings, and interest on partners’ loans at 5% per annum.

Limited companies

· Candidates must understand the features and accounting treatment of ordinary shares, bonus issues, rights issues, debentures, dividends, and reserves.

· Questions will not be set on preference shares.

· Prepare a statement of profit or loss, statement of financial position, and statement of changes in equity for a limited company.

· Limited company equity may include ordinary share capital, share premium, revaluation reserve, general reserve, and retained earnings.

· Dividends are distributions of profit to shareholders; they reduce retained earnings, not profit before tax.

· Debentures are long-term loans; interest on debentures is an expense in the statement of profit or loss.

· Candidates may need to choose suitable sources of finance for specified purposes.

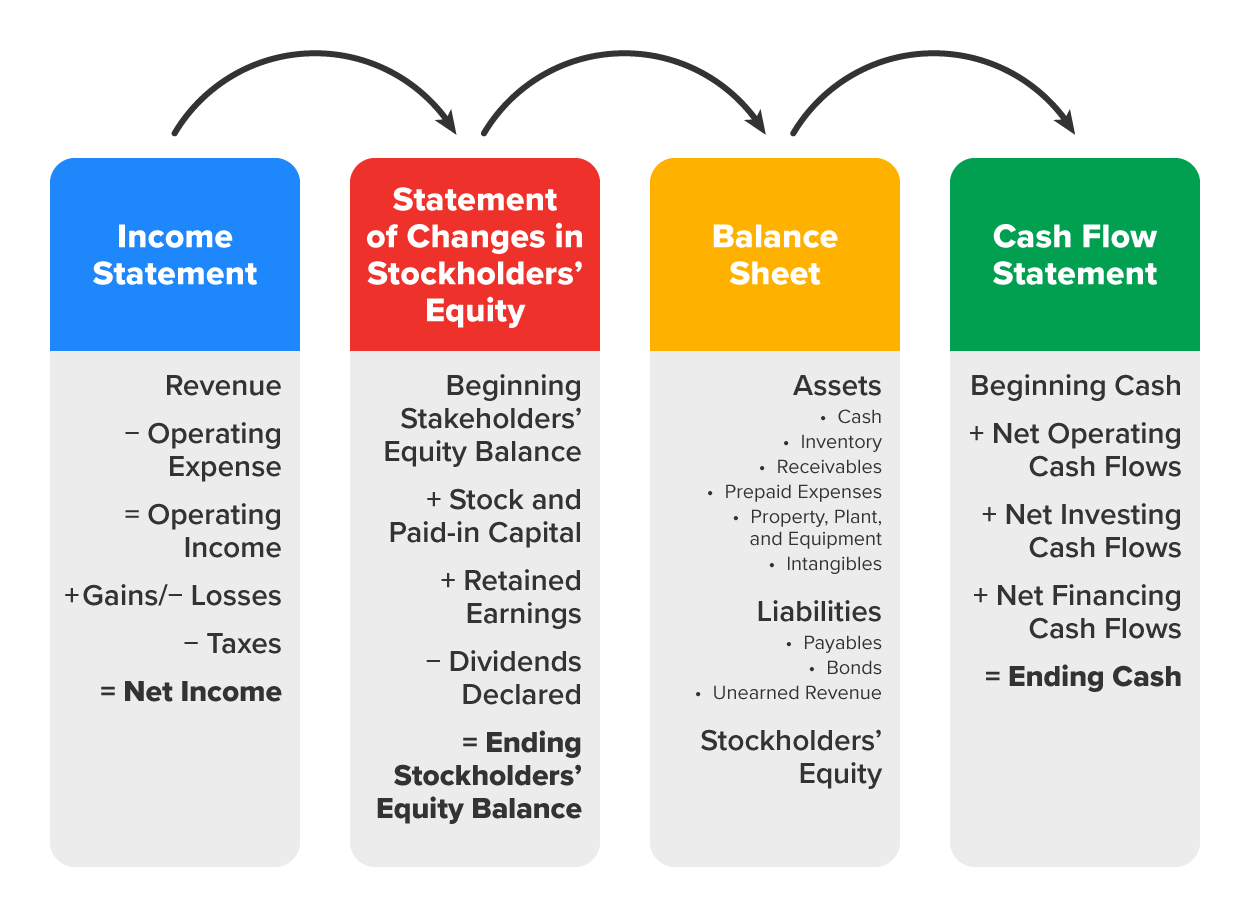

This part of the diagram shows how equity changes during the year. It links well to limited company accounts because it shows how share capital, retained earnings, and dividends affect closing equity. Source

Share issues and reserves

· Ordinary shares issued at par: debit bank, credit ordinary share capital.

· Ordinary shares issued at a premium: credit ordinary share capital with par value and share premium with the excess.

· Rights issue: existing shareholders are offered new shares, often at a favourable price. It raises cash for the company.

· Bonus issue: free shares issued to existing shareholders by capitalising reserves; it does not raise cash.

· For bonus issues, the syllabus states the revaluation reserve is not to be used.

· Capital reserves: share premium and revaluation reserve.

· Revenue reserves: retained earnings and general reserve.

· Exam skill: explain the advantages and disadvantages of bonus issues, rights issues, issuing shares, and issuing debentures from both company and shareholder viewpoints.

Statement formats: exam structure

· Statement of profit or loss: shows financial performance over a period.

· Statement of financial position: shows assets, liabilities and capital/equity at a specific date.

· Appropriation account: used for partnerships to divide profit or loss between partners.

· Statement of changes in equity: used for limited companies to show movements in share capital and reserves.

· Use correct labels: profit for the year, drawings, capital, current accounts, retained earnings, reserves, ordinary share capital.

· Keep layouts neat: headings, dates, columns, subtotals and final totals must be clear.

· Apply adjustments before finalising statements; do not leave draft trial balance figures unadjusted.

Common exam traps

· Treating drawings as an expense — drawings reduce owner’s capital, not profit.

· Forgetting to adjust both sides of an item, e.g. depreciation expense and accumulated depreciation.

· Putting prepayments as expenses instead of current assets.

· Putting accruals as current assets instead of current liabilities.

· Deducting dividends in the statement of profit or loss instead of from retained earnings.

· Sharing partnership profit before adjusting for interest on drawings, interest on capital, and partners’ salaries.

· Using the revaluation reserve for a bonus issue, which the syllabus excludes.

Checklist: can you do this?

· Calculate and record adjustments for accruals, prepayments, irrecoverable debts, depreciation, inventory valuation and errors.

· Prepare financial statements for sole traders, including from incomplete records.

· Prepare partnership accounts, including the appropriation account, capital accounts and current accounts.

· Apply partnership agreement rules and the Partnership Act 1890 where relevant.

· Prepare limited company statements and account for ordinary shares, rights issues, bonus issues, debentures, dividends and reserves.