Reconciliation and Verification: Purpose

· Reconciliation = comparing two related records to identify and explain differences.

· Verification = checking accounting records against supporting documents to confirm accuracy.

· Internal sources include cash book, sales ledger, purchases ledger, control accounts, journals, and ledger accounts.

· External sources include bank statements, supplier statements, customer remittance advices, invoices, and credit notes.

· Main purpose: detect errors, omissions, fraud risks, timing differences, and incorrect ledger balances before preparing final accounts.

Benefits and Limitations of Reconciliation and Verification

· Benefits: improves accuracy, detects missing entries, supports internal control, reduces risk of fraud, and increases confidence in financial statements.

· Helps management make better decisions using reliable accounting information.

· Provides evidence for correcting records before preparing the statement of profit or loss and statement of financial position.

· Limitations: does not guarantee all errors are found, depends on the accuracy of source documents, can be time-consuming, and may not detect collusion or deliberate manipulation.

· Some differences are only timing differences, not errors, so they require explanation rather than correction.

Trial Balance

· Trial balance = list of ledger balances with debit balances and credit balances totalled separately.

· Purpose: checks whether total debits = total credits after double-entry posting.

· If totals disagree, there is likely an error affecting only one side, wrong side, or wrong amount.

· A balanced trial balance does not prove that accounts are error-free.

· Trial balance figures are used to help prepare financial statements, but errors must be corrected first.

Errors Affecting the Trial Balance

· These errors usually make total debits ≠ total credits.

· Single-entry error: only one side of a transaction is recorded.

· Wrong-side error: an amount is entered on the wrong side of an account.

· Incorrect amount on one side: debit and credit entries are made for different amounts.

· Casting error: ledger account or trial balance column is added incorrectly.

· Balance omission: a ledger balance is left out of the trial balance.

Suspense Account and Error Correction

· Suspense account = temporary account used when the trial balance does not agree.

· Difference in trial balance is placed in the suspense account until errors are found.

· If debit total is lower, enter difference on the debit side of suspense account.

· If credit total is lower, enter difference on the credit side of suspense account.

· Correct errors using journal entries and close the suspense account when the error is fully corrected.

· Exam tip: only errors that affect trial balance agreement usually involve the suspense account.

Errors Not Affecting the Trial Balance

· Error of omission: transaction completely left out of the books.

· Error of commission: entry made in the wrong account of the same class, e.g. wrong customer.

· Error of principle: entry made in the wrong type of account, e.g. treating capital expenditure as revenue expenditure.

· Error of original entry: wrong amount entered in both debit and credit accounts.

· Error of reversal: debit and credit entries are reversed.

· Compensating errors: two or more errors cancel each other out.

· These errors are dangerous because the trial balance still balances.

Effect of Correcting Errors on Financial Statements

· Correction may affect profit, assets, liabilities, capital/equity, or only ledger classification.

· If an expense was understated, correcting it will decrease profit.

· If income was understated, correcting it will increase profit.

· If an asset was overstated, correcting it will decrease assets in the statement of financial position.

· If a liability was omitted, correcting it will increase liabilities.

· Always state both effects if asked: effect on profit or loss and effect on statement of financial position.

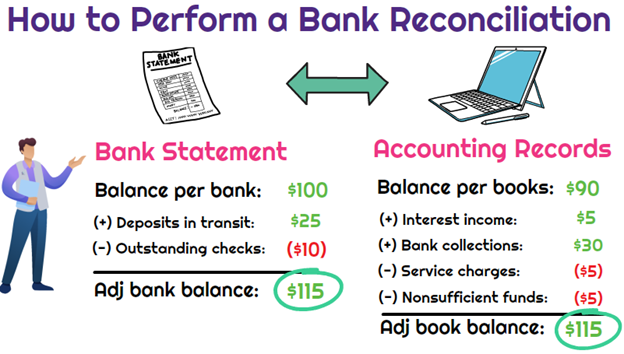

Bank Reconciliation Statements

· Bank reconciliation statement reconciles the cash book bank balance with the bank statement balance.

· First update the cash book for items already recorded by the bank but not yet recorded by the business.

· Common cash book updates: bank charges, bank interest, direct debits, standing orders, dishonoured cheques, credit transfers, and direct deposits.

· Then prepare the bank reconciliation statement for timing differences.

· Common timing differences: unpresented cheques and bank lodgements not yet credited.

· Unpresented cheque = cheque paid by business and entered in cash book, but not yet shown by the bank.

· Bank lodgement not yet credited = money received and entered in cash book, but not yet shown on bank statement.

This diagram shows how the bank statement balance is adjusted for timing differences. It is useful for remembering that not every difference is an error; some items have simply not appeared in both records yet. Source

Bank Reconciliation: Exam Method

· Step 1: Compare cash book with bank statement.

· Step 2: Tick matching items and identify differences.

· Step 3: Update cash book for bank-only items and cash book errors.

· Step 4: Start reconciliation with the updated cash book balance or the bank statement balance, depending on question format.

· Step 5: Adjust for unpresented cheques and lodgements not yet credited.

· Step 6: Final adjusted balance should agree with the other record.

Benefits and Limitations of Bank Reconciliation

· Benefits: detects errors in the cash book or bank statement, identifies fraud, confirms actual bank balance, and improves cash control.

· Helps ensure the bank balance in the statement of financial position is reliable.

· Limitations: does not detect all fraud, depends on accurate bank records, and only checks the bank account.

· Timing differences can make balances appear incorrect even when no error exists.

Control Accounts

· Control account = summary account in the general ledger used to check the accuracy of a detailed ledger.

· Sales ledger control account summarises transactions with credit customers / trade receivables.

· Purchases ledger control account summarises transactions with credit suppliers / trade payables.

· The control account balance should agree with the total of individual balances in the relevant ledger.

· If they disagree, prepare a reconciliation statement and correct errors.

· Control accounts help reduce the risk of errors in large ledgers with many customer or supplier accounts.

Sales Ledger Control Account

· Usually has a debit balance because customers owe money to the business.

· Debit entries may include credit sales, dishonoured cheques, and interest charged to customers.

· Credit entries may include receipts from customers, sales returns, discounts allowed, irrecoverable debts written off, and contra entries.

· Closing balance = total trade receivables shown in the statement of financial position.

· Errors in this account can affect assets, profit, or both.

Purchases Ledger Control Account

· Usually has a credit balance because the business owes money to suppliers.

· Credit entries may include credit purchases and refunds from suppliers.

· Debit entries may include payments to suppliers, purchases returns, discounts received, and contra entries.

· Closing balance = total trade payables shown in the statement of financial position.

· Errors in this account can affect liabilities, profit, or both.

Control Account Reconciliation Statements

· Used when the control account balance does not agree with the total of individual ledger balances.

· Start with one balance, then adjust for errors or omissions found in either the control account or the individual ledger accounts.

· Errors in the control account affect the general ledger and may affect financial statements.

· Errors only in individual customer/supplier accounts usually affect ledger detail, not the trial balance total.

· Reconciliation confirms whether the final corrected balances agree.

Benefits and Limitations of Control Accounts

· Benefits: detects errors, prevents fraud, provides quick totals for trade receivables and trade payables, and reduces work in checking individual accounts.

· Allows division of duties between staff maintaining the general ledger and staff maintaining personal ledgers.

· Limitations: does not identify every error, may not detect errors repeated in both the control account and personal ledger, and depends on accurate posting.

· A control account proves agreement between totals, not that every individual account is correct.

Checklist: can you do this?

· Explain why businesses use reconciliation and verification to improve accounting accuracy.

· Identify whether an error affects or does not affect the trial balance.

· Prepare journal entries and a suspense account to correct errors.

· Prepare an updated cash book and bank reconciliation statement.

· Prepare sales ledger control accounts, purchases ledger control accounts, and reconciliation statements.