AP Syllabus focus: ‘Price elasticity of supply depends on factors such as the price of alternative inputs.’

Price elasticity of supply explains how strongly producers adjust output when market price changes. This page focuses on the real-world conditions that make supply more or less responsive, especially input alternatives and production flexibility.

Core idea: responsiveness on the producer side

Elasticity of supply is about how easily firms can change quantity supplied when the good’s own price changes. The key determinants all operate through one question: how quickly and cheaply can producers expand (or contract) output without sharply increasing marginal cost?

Price elasticity of supply (PES)

Price elasticity of supply (PES): The percentage change in quantity supplied divided by the percentage change in price, holding other determinants of supply constant.

PES is unit-free and depends on production constraints, available technology, and input markets, not simply on the slope of a supply curve drawn on a graph.

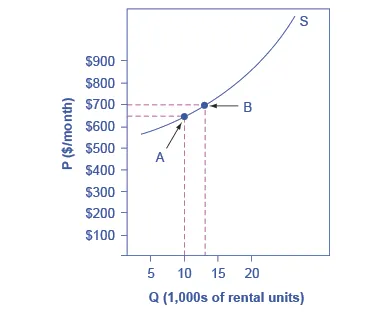

Supply curve for apartment rentals with two price–quantity points used to compute price elasticity of supply (PES). The dashed guides emphasize the changes in and that feed into the percent-change formula. This visual helps distinguish “elasticity” (a ratio of percentage changes) from the geometric slope of the curve. Source

PES = \dfrac{%\Delta Q_s}{%\Delta P}

= price elasticity of supply (unit-free)

= quantity supplied (units of output)

= price of the good (dollars per unit)

What determines elasticity of supply?

1) Time horizon (immediate, short run, long run)

Time is often the dominant determinant of PES because more time allows more adjustment margins.

Immediate/very short run: Supply tends to be inelastic.

Firms are stuck with current capacity, staffing, and inventories.

Short run: Supply becomes more elastic as firms can:

add shifts, pay overtime, reorder materials, intensify use of existing capital

Long run: Supply is typically more elastic because firms can:

build new plants, adopt new processes, enter/exit the industry, redesign products

2) Availability and price of alternative inputs (syllabus emphasis)

Producers combine inputs (labour, capital, raw materials, components).

Supply is more elastic when firms can switch among inputs without large cost increases.

If the price of alternative inputs is low (or falling), firms can expand output more easily because:

they can substitute toward relatively cheaper inputs

marginal cost rises more slowly as production increases

If the price of alternative inputs is high (or rising), supply is less elastic because:

scaling up requires expensive substitutions or bidding inputs away from other uses

marginal cost rises quickly, limiting responsiveness

This determinant is especially important when a key input is scarce or has few close substitutes (for example, a specialised component or location-specific resource).

3) Spare capacity and ability to vary utilisation

Spare capacity makes it easier to expand output when price rises.

More spare capacity → more elastic supply

idle machines, underused retail space, unused trucking capacity

Operating near full capacity → less elastic supply

expansion requires costly investment, maintenance delays, or congestion

4) Input mobility and factor specificity

Supply is more elastic when inputs can move into the industry quickly.

High mobility (generic labour skills, widely available materials) → higher PES

Specific factors (highly specialised labour, custom capital, unique land) → lower PES

Barriers such as licensing, training time, or geographic immobility reduce responsiveness.

5) Inventories and storability

If output can be stored and inventory exists, firms can respond more to price changes.

Large inventories/low storage cost → more elastic (release stock when price rises)

Perishability or expensive storage → less elastic

For many services, storage is impossible, which tends to reduce short-run elasticity.

6) Ease of scaling production and technological flexibility

Technology shapes how quickly marginal cost increases as output expands.

Flexible production processes (modular equipment, scalable software, standardised components) → higher PES

Rigid processes (fixed-proportion technologies, long setup times, bottleneck stages) → lower PES

Learning-by-doing and process innovation can increase PES over time by lowering adjustment costs.

7) Institutional and contractual constraints

Even when technically feasible, firms may be constrained by rules and agreements.

Long-term input contracts, union work rules, or scheduling constraints can reduce elasticity.

Regulations (permits, environmental compliance timelines) can slow expansion, lowering PES.

Conversely, streamlined permitting or flexible contracting can raise PES.

Common AP-level interpretations

Reading determinants without calculation

When asked to justify “more elastic” vs “more inelastic” supply, tie your reasoning to one or more of these mechanisms:

adjustment speed (time)

availability/cost of substitutable inputs (including the price of alternative inputs)

capacity limits

mobility of resources

inventory/storage feasibility

regulatory/contractual limits

Practice Questions

(2 marks) Explain how a fall in the price of an alternative input affects the price elasticity of supply of a good.

1 mark: States that supply becomes more elastic/more responsive (PES rises).

1 mark: Explains that cheaper alternative inputs make it easier/less costly to expand output when price rises.

(5 marks) A firm produces a good using specialised machinery and skilled labour. Analyse two factors that could make the firm’s supply more inelastic in the short run than in the long run.

1 mark: Identifies time horizon as a determinant (short run vs long run).

2 marks: Explains short-run constraints (e.g., fixed capacity/specialised capital, limited trained labour, contracts/regulation) reducing responsiveness.

2 marks: Explains long-run adjustments (e.g., invest in capital, train/hire labour, adopt new technology, entry/expansion) increasing responsiveness.

FAQ

They typically use input price indices, spot-market prices, or wage rates for substitute labour categories.

When inputs are bundled, analysts may model a cost function to infer which alternative input prices matter most.

Yes, if there are downward rigidities such as long-term contracts, minimum staffing requirements, or costs of shutting down and restarting.

Capacity can expand gradually but cannot be reduced without large losses, creating asymmetric responsiveness.

They may reallocate shared inputs (labour time, machine hours) across products.

If switching production lines is cheap, the product’s supply is more elastic; if retooling is slow or regulated, it is less elastic.

They can raise elasticity when firms can source inputs from many countries quickly.

They can lower elasticity when logistics bottlenecks, shipping capacity, or geopolitical risks make additional inputs hard to obtain on short notice.

Near capacity, marginal cost often rises sharply due to overtime premiums, maintenance issues, and congestion.

That steepening marginal cost is evidence of lower elasticity of supply at high utilisation rates.