Economics is a dynamic and evolving discipline that seeks to understand the complexities of how societies allocate their finite resources. This page delves deeper into the foundational meaning of economics, offers a comprehensive look at its varied perspectives, and differentiates between the realms of microeconomics and macroeconomics.

Basic Meaning

Economics, at its essence, is the study of how individuals, businesses, and governments make choices to allocate limited resources in an attempt to satisfy their boundless desires and needs.

- Scarcity: Every society faces the challenge of scarcity. Resources such as time, labour, and raw materials are finite, yet the demands for goods and services are virtually limitless. This imbalance necessitates the need for choices.

- Choice: At every level, from an individual deciding how to spend their income, to a government allocating its budget, choices are made. These decisions inherently involve trade-offs. The cost of any choice is the opportunity cost - the value of the next best alternative that is forgone.

Different Perspectives on the Study of Economics

Economics is a rich tapestry of ideas and theories. Over the centuries, thinkers have proposed various perspectives, each with its own interpretation of economic events and policies.

- Classical Economics: Originating from thinkers like Adam Smith and David Ricardo, classical economics champions the power of the free market. It posits that an 'invisible hand' guides economic activity, leading to beneficial outcomes when there's minimal government interference.

- Keynesian Economics: John Maynard Keynes revolutionised economic thought by arguing that in certain situations, especially during economic downturns, government intervention is essential to restore full employment and stability.

- Marxist Economics: Karl Marx presented a critique of capitalism, emphasising the disparities between the working class and the capitalists. He believed that capitalism would eventually lead to its own downfall, replaced by a socialist system.

- Neoclassical Economics: Building upon classical ideas, neoclassical economics focuses on how individuals make rational decisions to maximise their satisfaction or utility. It uses mathematical models to predict outcomes.

- Institutional Economics: This perspective emphasises the importance of societal structures, norms, and legal systems. It believes that institutions play a pivotal role in shaping economic outcomes.

- Developmental Economics: This branch is dedicated to understanding the economic phenomena of developing nations. It seeks solutions to challenges like poverty, infrastructure deficits, and education gaps.

- Environmental Economics: As concerns about the planet grow, this field analyses the economic impact of environmental policies and how economic activities affect the environment.

A summary table of different economic schools

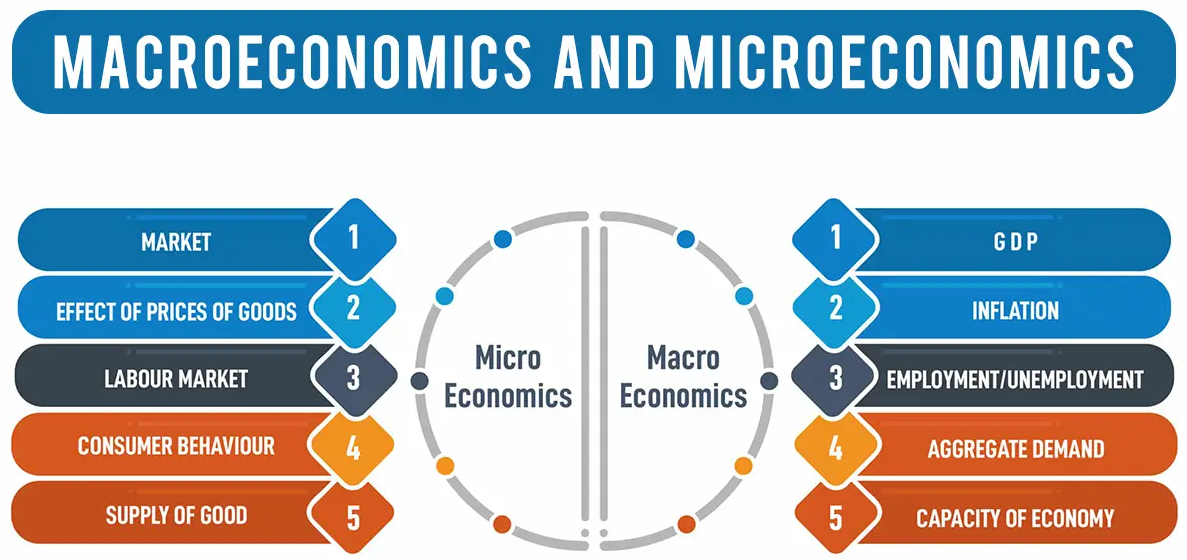

Microeconomics vs. Macroeconomics

Economics bifurcates into two primary branches: microeconomics and macroeconomics. Each offers a unique lens to interpret and understand economic activities.

Microeconomics

Microeconomics delves into the intricacies of individual entities such as consumers, firms, and specific markets. It's concerned with the mechanisms of supply and demand and the determination of prices and outputs in individual markets.

- Demand and Supply: The fundamental building blocks, these concepts analyse how prices are determined and how resources are allocated in individual markets.

- Elasticity: A crucial concept, elasticity gauges how sensitive quantity demanded or supplied is to changes in other economic variables, especially price.

- Consumer Behaviour: This area dives into the psyche of consumers, exploring how they make decisions based on preferences, incomes, and prices.

- Production and Costs: At the heart of business decisions, this examines how firms produce goods and services, the costs they incur, and how they decide on the optimal level of production.

Macroeconomics

Macroeconomics zooms out to look at the broader picture. It's concerned with the aggregate performance of the entire economy.

- National Income Accounting: This provides a statistical measure of a country's economic performance, most notably through indicators like Gross Domestic Product (GDP).

- Inflation: A key concern for policymakers, inflation represents the rate at which the general level of prices for goods and services rises, eroding purchasing power.

- Unemployment: Beyond just statistics, this delves into the human aspect of those out of work, the types of unemployment, and its various causes and effects.

- Monetary and Fiscal Policy: These are the primary tools governments and central banks use to influence the economy. While monetary policy deals with controlling the money supply and interest rates, fiscal policy involves government spending and taxation.

Image courtesy of studyiq

In navigating the vast world of economics, understanding its foundational definitions and distinctions is paramount. As you delve deeper, you'll find that whether it's the choices of an individual or the overarching policies of a nation, economics offers a structured way to interpret, analyse, and predict the myriad complexities of our financial world.

Practice Questions

Economics is the study of how individuals, firms, and governments make decisions to allocate limited resources in an attempt to satisfy their unlimited wants and needs. The discipline fundamentally addresses the issue of scarcity, which arises because resources such as time, labour, and raw materials are finite, yet the demands for goods and services are virtually limitless. This imbalance necessitates the need for choices. Every choice made involves an opportunity cost, which represents the value of the next best alternative that is forgone when a particular decision is made.

Microeconomics examines the behaviour of individual economic units, such as consumers, firms, and specific markets. It focuses on mechanisms of supply and demand, elasticity, consumer behaviour, and the production and costs associated with individual firms. On the other hand, macroeconomics looks at the economy as a whole, focusing on aggregate indicators and overarching economic policies. Key areas of macroeconomics include national income accounting, which measures the economy's overall performance, inflation, unemployment, and the study of monetary and fiscal policies that governments and central banks employ to influence overall economic activity.

FAQ

Economists rely heavily on data to test theories, understand current economic conditions, and make predictions. This data can come from a multitude of sources, including government reports, surveys, and international organisations. Economists use statistical tools and software to analyse this data, looking for patterns, relationships, and anomalies. For instance, they might use regression analysis to determine how different factors, like interest rates or consumer confidence, impact economic growth. While data is invaluable, it's also crucial for economists to recognise its limitations and the potential for biases, ensuring their analyses are as accurate and objective as possible.

Economics has undergone significant evolution since its inception. Early economic thought, rooted in philosophy, transitioned into a more structured discipline with the works of Adam Smith and David Ricardo. The Industrial Revolution further shaped economic theories, highlighting issues related to production, capital, and labour. The 20th century saw the rise of Keynesian economics, responding to the Great Depression, and later, the monetarist and neoliberal schools of thought. More recently, behavioural economics, which integrates psychological insights, has gained prominence. As global challenges like climate change and technological disruption emerge, economics continues to adapt, offering new perspectives and solutions.

While economics, business studies, and finance overlap in many areas, they have distinct focuses. Economics delves into the broader workings of economies, studying how resources are allocated among competing uses. It's concerned with understanding and predicting behaviour at both individual (micro) and aggregate (macro) levels. Business studies, on the other hand, concentrates on the operations and strategies of individual firms within the market. It looks at management, marketing, operations, and more. Finance is narrower still, focusing on the management of money and investments, looking at topics like asset valuation, risk management, and capital structures. Each offers a unique lens on the world of commerce and policy.

Opportunity cost is a foundational concept in economics because it captures the essence of scarcity and choice. Every decision made, whether by an individual, firm, or government, involves foregoing the next best alternative. This cost isn't always monetary; it can be time, resources, or any other factor of value. Recognising opportunity costs ensures that resources are used efficiently and that decisions are made with a clear understanding of their implications. For instance, if a government decides to invest in defence over education, the opportunity cost might be the potential long-term economic growth derived from a better-educated populace.

Economics, often dubbed the "dismal science", isn't always exact. It's grounded in theories and models that rely on assumptions. Different economists might prioritise different data, use varied models, or even hold contrasting fundamental beliefs about how economies work. For instance, a Keynesian economist might advocate for increased government spending during a recession, while a classical economist might argue for minimal intervention. Additionally, economics is influenced by societal, political, and cultural factors, leading to varied interpretations and recommendations. This diversity of thought, while sometimes confusing, enriches the discipline and fosters healthy debate.