Economic thinking is a systematic approach to understanding and analysing economic phenomena. It revolves around three core concepts: marginal analysis, the comparison of costs and benefits, and the role of incentives.

Marginal Analysis

Marginal analysis is a cornerstone of economic thought. It's the study of the effects of small changes, focusing on the incremental benefits or costs of a decision rather than the total or average.

Image courtesy of wallstreetmojo

Key Points:

- Marginal Benefit (MB): This refers to the additional satisfaction or utility that a consumer derives from consuming an additional unit of a good or service. It's a crucial concept because it helps determine how much of a product a consumer will buy.

- Marginal Cost (MC): This is the extra cost incurred by producing one more unit of a product. In the world of business, understanding MC is vital because it influences pricing and production levels.

- The principle of equi-marginal utility states that consumers will allocate their resources (like money) in such a way that the last unit of a good or service consumed provides the same level of marginal utility across all consumption choices.

Examples:

- Studying for Exams: If a student is contemplating whether to study an additional hour for an exam, they would weigh the marginal benefit (potential for a higher grade) against the marginal cost (loss of leisure time or sleep).

- Production Decisions: A manufacturer might weigh the marginal benefit of producing one more item (additional revenue from the sale) against the marginal cost (the cost of materials and additional labour for that item).

Costs vs. Benefits

Every economic decision involves a trade-off. By comparing the associated costs and benefits, one can make more informed decisions.

Image courtesy of wallstreetmojo

Key Points:

- Total Cost: This encompasses all costs, both fixed and variable, associated with an action or decision. It's essential for determining profitability and making budgetary decisions.

- Total Benefit: This is the sum of all the advantages or gains achieved from a particular action or decision. It can be tangible, like monetary gains, or intangible, like satisfaction or happiness.

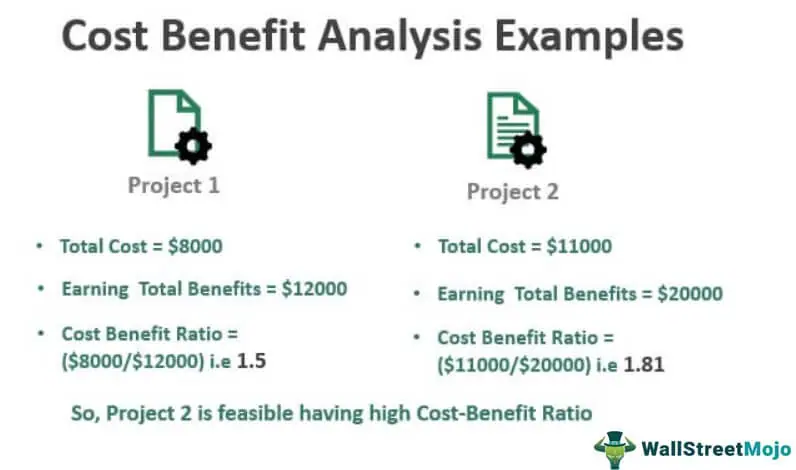

- Cost-Benefit Analysis: This is a systematic approach to estimate the strengths and weaknesses of alternatives. It's used to determine options that provide the best approach to achieve benefits while preserving savings.

- Sunk Costs: These are costs that have already been incurred and cannot be recovered. They should not influence future economic decisions as they are irrelevant to future costs and benefits.

Examples:

- University Education: When deciding to attend university, students might weigh the total benefits (like potential higher lifetime earnings, networking opportunities, and personal development) against the total costs (tuition fees, living expenses, and potential lost wages from not working).

- Public Projects: A local council might conduct a cost-benefit analysis before deciding to build a new community centre, comparing the benefits to the community against the financial costs of construction and maintenance.

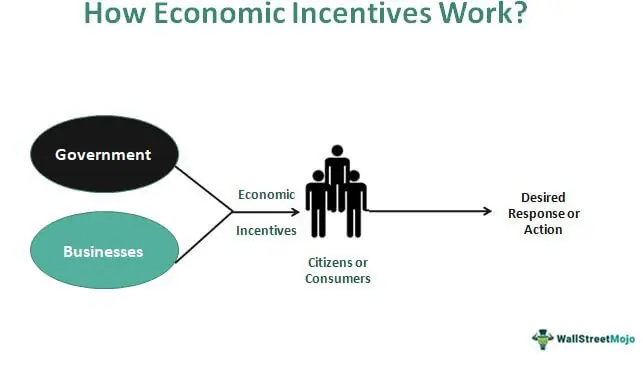

Role of Incentives

Incentives are fundamental to economic behaviour. They influence the choices individuals and firms make and can be both positive (rewards) and negative (penalties).

Image courtesy of wallstreetmojo

Key Points:

- Positive Incentives: These encourage a specific behaviour by offering rewards. They can be financial, like bonuses or discounts, or non-financial, like praise or recognition.

- Negative Incentives: These aim to deter certain behaviours by imposing penalties. They can be in the form of fines, sanctions, or even social disapproval.

- Unintended Consequences: Sometimes, incentives can lead to unexpected or undesired outcomes. For instance, a well-intentioned policy might create incentives for individuals or firms to behave in ways that weren't anticipated by policymakers.

- Incentive Compatibility: This is when the incentives for all parties in a transaction align with the overall objectives. It ensures that each party has a reason to participate in the transaction and act as desired.

Examples:

- Environmental Policies: Governments might offer tax incentives or grants to companies that invest in green technologies, making it more economically attractive to be environmentally friendly.

- Behavioural Economics: Loyalty programmes in retail are positive incentives, encouraging repeat purchases by offering points or discounts.

- Law Enforcement: Fines for littering or not wearing a seatbelt are negative incentives, discouraging undesired behaviours.

In essence, economic thinking, with its focus on marginal analysis, costs vs. benefits, and the role of incentives, equips individuals and institutions with the tools to navigate the complexities of decision-making. By understanding these foundational concepts, one can make choices that are more informed, rational, and beneficial in the long run.

Practice Questions

Marginal analysis focuses on evaluating the additional benefits or costs associated with a decision. In economic decision-making, it's essential because it helps individuals and firms determine the value of pursuing an additional unit of an action, be it consumption, production, or any other economic activity. By comparing the marginal benefit (MB) to the marginal cost (MC), one can decide whether the action is beneficial. If MB exceeds MC, then the action is considered economically rational. This principle aids in optimising resource allocation, ensuring that decisions lead to the highest possible level of utility or profit.

Incentives play a pivotal role in shaping economic behaviour. Positive incentives, such as bonuses or discounts, encourage specific actions by offering rewards. They motivate individuals or firms to behave in ways that align with the incentive's objective. On the other hand, negative incentives, like fines or sanctions, deter undesired behaviours by imposing penalties. For instance, tax breaks might incentivise companies to invest in renewable energy, while fines can discourage illegal dumping. Both types of incentives alter the perceived costs and benefits of actions, guiding behaviour towards desired economic outcomes. They are instrumental tools for policymakers and businesses alike to influence decisions and achieve specific objectives.

FAQ

Externalities refer to the unintended side effects of an economic activity that affect third parties who did not choose to be involved in that activity. These can be positive (benefits) or negative (costs). In economic thinking, when externalities are present, the private costs or benefits (borne by the individuals or firms involved in the activity) do not reflect the true societal costs or benefits. For instance, a factory that pollutes a river might have low production costs but imposes high societal costs due to environmental damage. Traditional cost-benefit analysis might miss these external effects. Therefore, for a comprehensive understanding, it's crucial to account for externalities to ensure that decisions lead to the overall welfare of society.

The principle of equi-marginal utility is central to understanding consumer choice. It states that consumers will allocate their resources in such a way that the last unit of a good or service consumed provides the same level of marginal utility across all consumption choices. In simpler terms, consumers aim to get the most "bang for their buck". If one good offers higher marginal utility per unit of currency than another, the consumer will buy more of the first good until the marginal utilities equalise. This principle ensures that consumers maximise their total utility given their budget constraints, leading to optimal consumption patterns.

Economic thinking often assumes that individuals have perfect information and ample time to make decisions. However, in reality, individuals often face information and time constraints. Limited information can lead to decisions based on heuristics or rules of thumb, which might not always be optimal. Time constraints can lead to impulsive decisions or choices based on immediate gratification rather than long-term benefits. These constraints challenge the traditional notions of rationality and optimal decision-making in economic thinking. Recognising these limitations is essential for a more realistic and holistic understanding of economic behaviour in real-world scenarios.

Behavioural economists challenge the traditional economic assumption that individuals are always rational and act in their best interest. They argue that cognitive biases, emotions, and social factors can influence decision-making, leading individuals to make choices that might seem irrational from a classical economic perspective. For instance, the concept of "loss aversion" suggests that people feel the pain of a loss more acutely than the pleasure of a similar gain, which can influence their decisions. While traditional economic thinking assumes perfect rationality, behavioural economics provides a more nuanced understanding, acknowledging the psychological complexities involved in real-world decision-making.

Sunk costs refer to costs that have already been incurred and cannot be recovered. In economic thinking, especially in decision-making, sunk costs should be ignored because they are irrelevant to future costs and benefits. For instance, if a business has spent money on a marketing campaign that didn't yield expected results, that expenditure is a sunk cost. When deciding on future marketing strategies, this past cost should not influence the decision. Instead, the focus should be on marginal costs and benefits. Recognising and disregarding sunk costs helps in avoiding the "sunk cost fallacy", where individuals or businesses continue a behaviour based on previously invested resources, rather than evaluating the current and future value of decisions.