AP Syllabus focus: ‘Economic costs include both explicit costs and implicit opportunity costs when comparing alternatives.’

Economic decisions require measuring the full cost of using scarce resources. This page distinguishes explicit and implicit costs and shows how including both changes what “profit” and “cost” mean in microeconomic analysis.

Why economists separate costs

Firms use inputs that may require a cash payment, or may be supplied by the owner without a direct payment. Both are costs because both use resources that have alternative uses. Ignoring non-cash costs can make an option look cheaper than it really is.

Explicit costs (accounting costs)

Explicit costs are straightforward because they appear as out-of-pocket payments and are recorded in financial accounts.

Explicit cost: A monetary payment a firm makes to purchase or hire resources (for example, wages, rent paid to a landlord, utility bills, or payments for raw materials).

Explicit costs matter for:

Cash flow (whether the firm can pay its bills)

Accounting profit calculations used in financial reporting

Many real-world business decisions that are constrained by available cash

Typical explicit costs include:

Wages paid to workers

Rent paid for a storefront or factory

Interest paid on borrowed funds

Payments to suppliers for parts and inventory

Advertising and insurance premiums

Implicit costs (opportunity costs of owned resources)

Some resources used by the firm are not purchased on the market because they are already owned by the entrepreneur or shareholders. Using them still creates a cost: the value of the next-best alternative that is given up.

Implicit cost: The opportunity cost of using resources owned by the firm (or owner) rather than renting them out, selling them, or employing them in the next-best alternative.

Implicit costs commonly arise from:

Owner’s time and labor: the salary the owner could earn working elsewhere

Owner-supplied capital: the return the owner could earn by investing funds in the next-best alternative

Owner-owned property: the rent the firm could earn by leasing the building or land to someone else

Entrepreneurial ability: the market value of the owner’s management in another job or business

Economists treat implicit costs as real because they capture the trade-off created by scarcity: choosing one use of a resource necessarily means forgoing another use.

Economic cost: combining explicit and implicit costs

For AP Microeconomics, the key idea is that economic cost includes both the cash payments the firm makes and the opportunity costs of self-owned resources. This allows comparisons across alternatives on a consistent basis, even when one option involves fewer recorded expenses.

Economic cost: The total opportunity cost of production, equal to explicit costs plus implicit costs.

Including implicit costs changes how profit is interpreted.

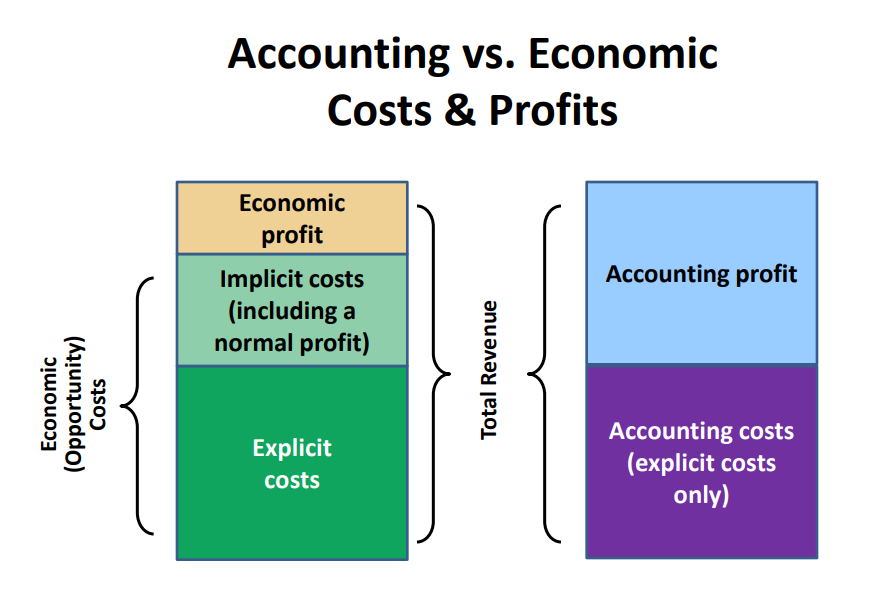

This diagram decomposes total revenue into explicit costs and implicit costs (including normal profit), making it easy to see why economic profit is smaller than accounting profit when implicit costs are counted. It visually reinforces that accounting profit subtracts only explicit (out-of-pocket) costs, while economic profit subtracts the full opportunity cost of resources used. Source

A firm can appear profitable in accounting terms but have low or even negative economic profit once the owner’s forgone alternatives are counted.

= Profit after subtracting all opportunity costs, in dollars per period

= Total sales receipts, in dollars per period

= Out-of-pocket payments, in dollars per period

= Forgone earnings from next-best alternatives, in dollars per period

This distinction helps explain why firms may:

Stay in business even with low accounting profit (if implicit costs are low)

Exit despite positive accounting profit (if implicit costs are high)

Reallocate resources when better alternatives become available

Recognising implicit costs in practice

Implicit costs are not directly observed as transactions, so they must be inferred from the best available alternative. The best alternative is usually measured using a market benchmark:

Market wage for similar work (for owner labor)

Market rent for similar property (for owner-owned space)

Market interest/return for similar risk (for owner capital)

A good rule: if a resource is owned and used by the firm, ask, “What income could this resource earn in its next-best use?” That forgone income is the implicit cost.

Common pitfalls (what AP expects you to avoid)

Treating implicit costs as “not real” because no cash changes hands; in economics they are real opportunity costs.

Double-counting: if the firm actually pays rent to a landlord, that rent is explicit, not implicit.

Using irrelevant alternatives: implicit cost must be based on the next-best feasible option, not a far-fetched or impossible one.

Mixing perspectives: costs depend on whose decision is being analyzed (the firm/owner), so the relevant forgone alternatives must match that decision-maker.

Practice Questions

(3 marks) Define explicit cost and implicit cost, and state one example of each.

1 mark: Explicit cost defined as an out-of-pocket monetary payment for resources.

1 mark: Implicit cost defined as the opportunity cost/forgone income from using owner-owned resources.

1 mark: One correct example for each (e.g., wages/rent paid as explicit; forgone salary/forgone rent as implicit).

(6 marks) A sole trader uses a building they own for their business and does not pay themselves a salary. They also pay cash wages to employees and pay for materials.

(a) Identify two explicit costs and two implicit costs in this situation. (4 marks)

(b) Explain how including implicit costs affects the comparison between accounting profit and economic profit. (2 marks)

1 mark each (up to 2): Explicit costs identified (e.g., cash wages to employees; materials).

1 mark each (up to 2): Implicit costs identified (e.g., forgone rental income from the owned building; forgone wage/salary of the owner). (b)

1 mark: Accounting profit subtracts explicit costs only; it omits implicit costs.

1 mark: Economic profit subtracts both explicit and implicit costs, so it is lower than (or equal to) accounting profit.

FAQ

They typically use the return on the closest comparable investment with similar risk.

Possible benchmarks include:

A market interest rate for low-risk funds

An expected rate of return in the same industry for similar risk

The key is consistency: use the best next-best alternative available to that owner.

Depreciation is usually treated as an accounting (non-cash) charge reflecting capital wearing out.

Economically, the underlying idea aligns with opportunity cost: using capital today reduces its future value. How it is classified can depend on context, but it is not an out-of-pocket payment like wages or materials.

Because the owner may be giving up a better alternative, such as:

A higher-paid job elsewhere

Renting out a property instead of using it

Investing their funds for a higher return

Once these forgone alternatives are counted as implicit costs, economic profit may be negative.

Only if leisure is the next-best alternative that would be chosen. If the realistic alternative to running the business is leisure (rather than paid employment), then the opportunity cost may include the value the owner places on forgone leisure, though it is harder to measure.

Implicit costs are opportunity costs that depend on the choice being made now (they are relevant to comparing alternatives).

Sunk costs are past, unrecoverable costs that do not change with the current decision.