AP Syllabus focus: ‘The value-added approach calculates GDP by summing the value added at each stage of production.’

The value-added approach is a practical method for measuring output that tracks how production increases a good’s worth across stages. It is especially useful for understanding why GDP counts final production once, not repeatedly.

Core Idea of the Value-Added Approach

The value-added approach measures GDP by adding up the additional value created at each step of production, from raw materials to the final sale. The goal is to count production without accidentally counting the same output multiple times.

Why “Value Added” Matters

At each stage, firms buy inputs, transform them, and sell outputs. The difference between what a firm sells and what it buys from other firms reflects that firm’s contribution to total production.

Value added: The market value a firm creates by producing output minus the value of intermediate inputs it purchases from other firms.

Value added aligns with how production actually occurs in supply chains and helps students see GDP as the sum of productive contributions rather than the sum of all sales receipts.

Intermediate vs Final Goods (and the Double-Counting Problem)

GDP is intended to measure the value of final goods and services produced in a time period. If economists simply summed all sales at every stage, they would overstate output.

Intermediate good: A good or service purchased for further processing or resale as part of producing another good, rather than for final use.

To avoid overstating GDP, the value-added approach includes each intermediate stage’s contribution once, ensuring the final total equals the value of the final product (when consistently measured).

How the Value-Added Method Is Computed

Conceptually, you move along the production chain and compute value added for each firm (or production stage), then sum those value-added amounts to obtain GDP.

General Steps (No Calculations Required)

Identify the main stages of production for a product (e.g., raw materials, processing, manufacturing, retail).

For each stage, determine:

Value of output (sales revenue) from that stage

Cost of intermediate inputs purchased from other firms

Compute value added at each stage.

Sum value added across all stages to obtain GDP for that product (and then across all products in the economy).

This approach works best when intermediate purchases can be distinguished from purchases of final goods.

= value created at a production stage, measured in dollars

= sum of value added across all production stages within the economy, measured in dollars

What the Value-Added Approach Helps You Understand

It Prevents Double Counting

Double counting occurs when the same production is included more than once (for example, counting both the value of flour sold to a bakery and the value of bread sold to consumers). Value added ensures only the incremental contributions are counted.

It Connects Production to Incomes Paid by Firms

Although this page focuses on value added, it is useful to interpret value added as the pool from which firms pay:

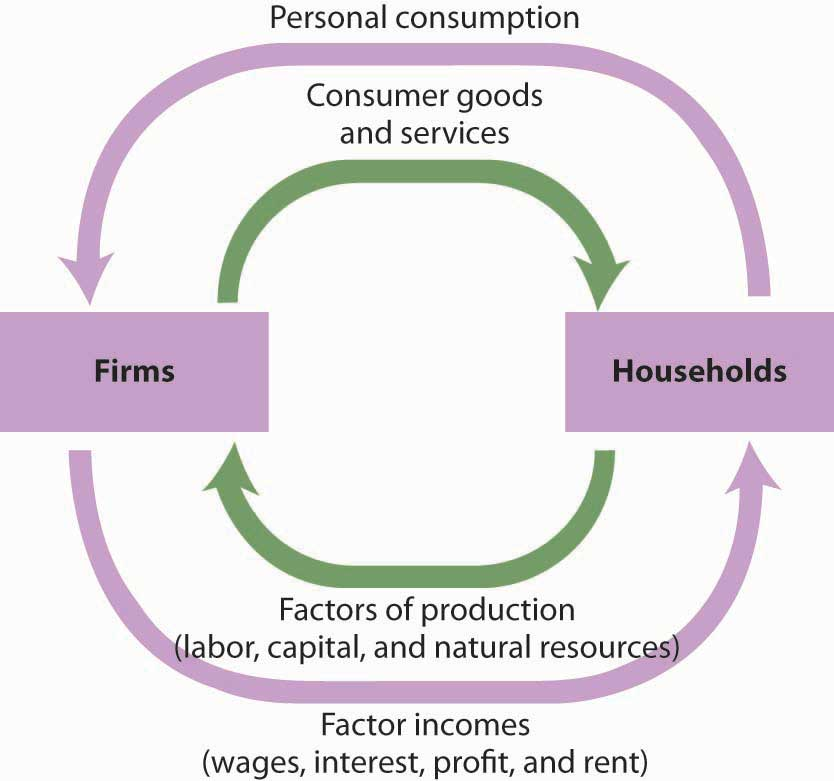

Circular-flow diagram showing firms purchasing factor services from households and paying factor incomes in return, while households purchase final goods and services from firms. This is a visual reminder that production (and value added) is mirrored by income earned by households via wages, rent, interest, and profit. Source

Wages and salaries to labour

Rent to owners of land/property

Interest to lenders

Profit to entrepreneurs/shareholders

This interpretation reinforces that GDP is tied to real production happening at each stage, not just the final transaction.

It Handles Complex Supply Chains

Modern goods often pass through many firms. Summing value added:

accommodates multiple suppliers and subcontractors

avoids needing to classify every item strictly as “final” at the moment of sale

provides a consistent way to measure production when firms sell both to other firms and to consumers

Practice Questions

Question 1 (3 marks) Explain how the value-added approach avoids double counting when measuring GDP.

Defines or identifies double counting as counting the same output more than once. (1)

Explains that intermediate purchases are subtracted from a firm’s sales/output to isolate that firm’s contribution. (1)

States that summing value added across stages equals the value of the final good and therefore counts output once. (1)

Question 2 (6 marks) Describe the steps an economist would take to measure GDP for a product using the value-added approach, and explain how value added at each stage relates to payments to factors of production.

Identifies that production is broken into stages/firms along the supply chain. (1)

States that the value of output (sales) is found for each stage. (1)

States that the cost/value of intermediate inputs purchased is identified for each stage. (1)

Explains that value added is computed as output minus intermediate inputs. (1)

Explains that GDP is the sum of value added across all stages. (1)

Links value added to factor payments (e.g., wages, rent, interest, profit) funded by the value created at that stage. (1)

FAQ

Yes. If a firm sells output for less than the cost of intermediate inputs (e.g., heavy discounting or spoilage), measured value added can be negative.

In national accounts, persistent negatives may signal measurement issues, unusual market conditions, or timing problems in recording sales versus input purchases.

A retailer typically adds value through distribution services (convenience, location, product assortment). Its value added is the retail sales revenue minus the wholesale cost of goods purchased.

This highlights that services can generate value added even without physically transforming goods.

They can. A domestic firm’s value added subtracts the cost of intermediate inputs regardless of origin, so only the domestic contribution remains in domestic GDP.

This prevents foreign production embodied in imported inputs from being counted as domestic output.

In industries with many business-to-business transactions (e.g., manufacturing networks), tracking final goods alone can be difficult.

Value-added reporting by firms can be more reliable because it focuses on each firm’s own contribution rather than tracing every input to its final use.

Firms usually compute value added at the firm level: total revenue from outputs minus total spending on intermediate goods and services.

For detailed industry analysis, statisticians may allocate intermediate costs across product lines using accounting rules or survey-based estimates.