AP Syllabus focus: ‘The main phases of the business cycle are expansion and recession.’

The business cycle describes recurring ups and downs in overall economic activity. For AP Macroeconomics, focus on how the two main phases—expansion and recession—affect output, jobs, and prices.

The Two Main Phases

Expansion

Expansion: a phase of the business cycle in which real GDP rises and the overall level of economic activity increases.

In an expansion, the economy is generally moving toward higher production and greater use of resources.

Output and income: Firms increase production; household incomes tend to rise with stronger labor demand.

Employment: Unemployment tends to fall as hiring increases and layoffs slow.

Spending and confidence: Consumers and firms are typically more willing to spend and invest when future income and sales look stronger.

Capacity pressures: As the economy runs closer to full use of resources, firms may face bottlenecks (labour shortages, capacity limits), which can influence prices and wages.

A key idea is that expansions are often reinforced by feedback loops: rising income supports spending, which supports production and employment.

Recession

A recession is the contractionary phase when overall activity declines rather than grows.

Recession: a phase of the business cycle in which real GDP falls and the overall level of economic activity decreases.

Recessions reflect economy-wide weakness that can spread across many industries.

Output and income: Firms cut production when sales drop; household income growth slows or turns negative for some workers.

Employment: Unemployment tends to rise due to layoffs, reduced hours, and slower hiring.

This chart plots the unemployment rate over time with recessions shaded in gray. The spikes that occur during shaded intervals illustrate how recessions are typically associated with rising unemployment, while expansions are usually periods of falling or stable unemployment. It supports the “output–jobs” linkage emphasized in business-cycle analysis. Source

Spending and confidence: Lower confidence can reduce consumer purchases (especially durable goods) and discourage business investment.

Inflation conditions: Price pressures often ease as demand weakens, though inflation outcomes depend on what is happening to costs and supply conditions.

Recessions can also be self-reinforcing: job losses reduce income, which reduces spending, which further reduces sales and production.

How Expansions and Recessions Show Up in Core Indicators

Real GDP and overall activity

In expansion, real GDP typically grows faster and more broadly across sectors.

In recession, real GDP declines as firms experience weaker demand and reduce output.

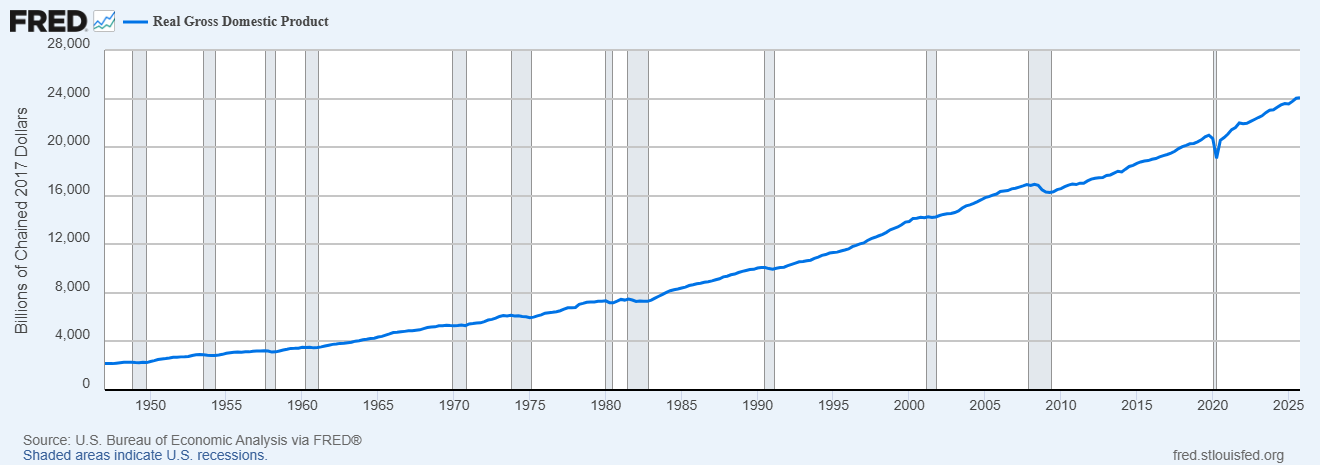

This time-series plot tracks real GDP growth over time and highlights recession periods with gray shading (as dated by the NBER). The negative growth rates that cluster in shaded regions illustrate the contractionary phase of the business cycle, while sustained positive growth is characteristic of expansion. It’s a clean way to connect the concept of “real GDP rises/falls” to actual historical data. Source

Labour market patterns

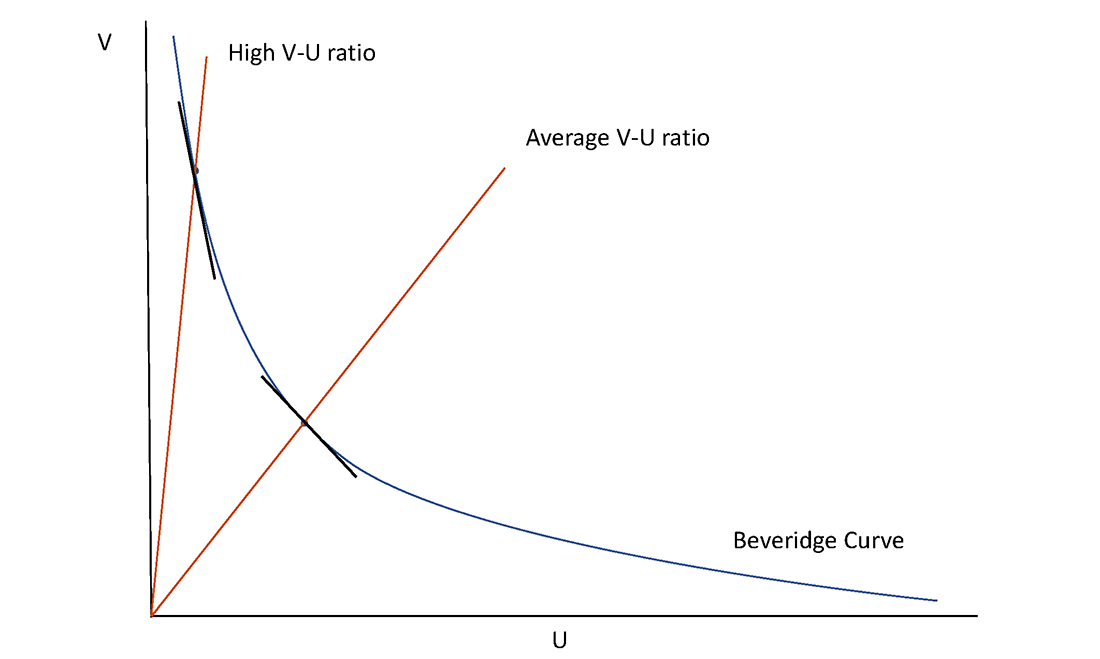

This stylized Beveridge Curve shows the inverse relationship between the unemployment rate () and job vacancies (). Points associated with expansions tend to feature relatively low unemployment and higher vacancies, while recessions tend to feature higher unemployment and lower vacancies. The “high V–U ratio” versus “average V–U ratio” rays emphasize that labor markets can look very different depending on where the economy is in the cycle. Source

In expansion, stronger demand for labour tends to reduce unemployment and increase hours worked.

In recession, weaker demand for goods and services lowers derived demand for labour, raising unemployment and reducing hours.

Price level pressures (broad patterns)

In expansion, stronger spending can increase inflationary pressure if production cannot keep up smoothly.

In recession, inflationary pressure often diminishes because households and firms cut back on spending; however, inflation can behave differently if cost shocks or supply disruptions are present.

Why These Phases Matter for Policy and Decision-Making

Understanding the two phases helps interpret economic news and policy actions:

During expansion, policymakers may watch for overheating risks (rapid price or wage growth) and financial imbalances.

During recession, policymakers often focus on stabilising output and employment by supporting spending and restoring confidence.

These phases provide a simple but powerful framework for connecting changes in spending, production, and employment to overall macroeconomic performance.

Practice Questions

(2 marks) State the two main phases of the business cycle and identify which phase is associated with rising real GDP.

Names expansion and recession (1)

Identifies expansion as the phase with rising real GDP (1)

(6 marks) Explain how an economy’s unemployment and inflationary pressure are likely to change as it moves from recession into expansion.

Unemployment is likely to fall in expansion due to increased hiring/higher derived demand for labour (2)

Mentions that inflationary pressure is likely to rise or become more likely in expansion as spending strengthens and capacity constraints can emerge (2)

Provides a coherent explanation linking stronger demand/production to labour market improvement and price pressures (2)

FAQ

They use a range of indicators rather than a single rule.

Common criteria include:

Breadth: weakness across many sectors

Duration: decline lasting more than a very short period

Depth: sizable drops in output, jobs, and incomes

Different countries rely on different statistical agencies or independent panels.

Inflation can be driven by costs as well as demand.

Examples include:

Supply disruptions that reduce availability of key inputs

Currency depreciation raising import prices

Energy or food price spikes

In these cases, weak demand may not fully offset higher production costs.

Yes. Wage growth depends on productivity and labour market conditions.

If:

Productivity is weak, or

Labour supply is growing quickly, or

Bargaining power is limited,

then employment and output can rise while wages grow slowly in real terms.

Length varies with:

Financial stability (credit booms can end abruptly)

Policy choices (timely stabilisation can extend expansions)

Productivity and innovation trends

External shocks (wars, energy shocks, global downturns)

No single factor determines duration.

A double-dip occurs when the economy enters recession, begins to recover briefly, and then falls back into recession again.

It often reflects:

Premature tightening of policy

Renewed financial stress

A fresh external shock disrupting the recovery