AP Syllabus focus: ‘Consumers face constraints and are assumed to make optimal decisions within those limits.’

Consumers cannot have everything they want, so microeconomics begins with the idea that choices are made under limits. This page explains how constraints shape decisions and what economists mean by rational choice.

Core idea: constraints + choice

Economists model consumer behavior with two linked assumptions:

Consumers face constraints that restrict feasible options.

Consumers make optimal choices among feasible options, given their goals and information.

What is a consumer constraint?

A consumer constraint is any limit that prevents consumption bundles from being freely chosen. The most important is the budget constraint, but time, rules, and access can also matter.

Budget constraint: The set of bundles of goods and services a consumer can afford given income, prices, and required payments (like taxes).

A budget constraint divides options into:

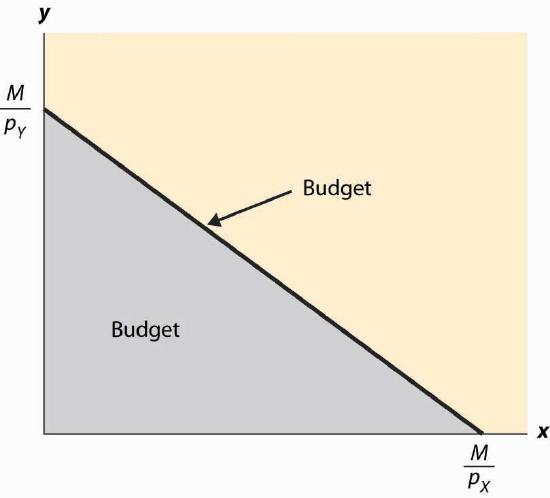

A standard budget-set diagram: the shaded region is the feasible (affordable) set and the straight boundary is the budget line where the consumer exactly exhausts the budget. It also visually separates feasible bundles from infeasible bundles above/outside the constraint and highlights the intercepts (all income spent on one good vs. the other). Source

Affordable (feasible): bundles within income.

Unaffordable (infeasible): bundles that exceed income.

The budget line and what it means

For two goods, the budget line shows combinations that exhaust the budget. Its slope reflects the trade-off imposed by market prices.

= price of good (dollars per unit)

= quantity of good (units)

= price of good (dollars per unit)

= quantity of good (units)

= consumer income or budget (dollars)

Because money spent on one good cannot be spent on another, the budget line captures scarcity at the individual level: choosing more of one good requires choosing less of another.

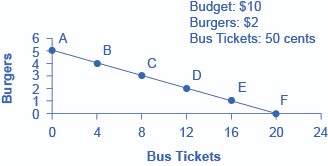

A budget-constraint graph using a concrete two-good example (burgers vs. bus tickets) with labeled endpoints and intermediate bundles along the line. The downward slope illustrates the opportunity cost trade-off implied by prices: moving toward more of one good necessarily reduces the maximum affordable amount of the other. Source

Rational choice as “optimal within limits”

The AP framing is: consumers “are assumed to make optimal decisions within those limits.” This is not a claim that consumers are perfect; it is a modelling approach.

Rational choice: Selecting the feasible option that best achieves the consumer’s objective (typically highest satisfaction) given constraints and the information the consumer uses.

Key features of this assumption:

Goal-directed: choices are consistent with an objective (often “more is better,” but not always).

Constraint-respecting: the chosen bundle must be affordable and permitted.

Consistent trade-offs: if a consumer prefers A to B when both are feasible, that ranking does not flip without a change in preferences or information.

Feasible set vs. preferred set

Think of decision-making in two layers:

Feasible set: what the consumer can choose (constraint-determined).

Preferred set: what the consumer wants to choose (preference-determined).

Rational choice predicts the consumer selects the most preferred option inside the feasible set, not the most preferred option overall.

Types of constraints relevant to consumers

Income and prices (the standard constraint)

The central constraint in consumer theory is limited income relative to prices. Changes shift or rotate the budget line:

Income changes shift the budget line outward/inward (more/less affordability).

Price changes rotate the budget line (the good that becomes cheaper becomes relatively easier to afford).

Time constraints

Time can limit consumption even when money is available (e.g., commuting time, waiting, hours in the day). In modelling, time constraints often act like an additional “budget,” restricting feasible bundles of activities.

Institutional and access constraints

Rules and access can constrain choice:

Age restrictions, rationing rules, membership requirements

Credit availability or purchase limits

Geography (no nearby suppliers) or inventory shortages

These constraints matter because rational choice is always evaluated within the set of options actually available.

How economists use the assumption

The constraint-plus-optimization approach helps predict how choices respond to changes in the environment:

If a constraint tightens (lower income, higher required payments), the feasible set shrinks, and the optimal choice may change.

If a constraint relaxes (higher income, lower prices), the feasible set expands, enabling higher attainment of the consumer’s objective.

This logic underpins many AP Micro applications: when incentives change via prices or policy, consumer choices change because the constraints and trade-offs change.

Common pitfalls for AP students

Confusing preferences with constraints: “I can’t afford it” is a constraint; “I don’t like it” is a preference.

Assuming rational choice means “selfish” or “always monetary”: rationality is about goal achievement, whatever the goal is.

Ignoring feasibility: an “optimal” bundle must satisfy the budget constraint and any other binding limits.

Practice Questions

(2 marks) Explain what economists mean when they assume consumers make “optimal decisions within constraints”.

1 mark: Identifies a constraint (e.g., limited income and given prices defining what is affordable).

1 mark: Explains optimality as choosing the best/most preferred feasible option (not necessarily the overall most preferred option).

(6 marks) A consumer buys two goods, and , with income . (a) State the budget constraint and define each variable. (b) Using the idea of rational choice, explain how the budget constraint affects what the consumer will choose.

(a) 3 marks:

1 mark: Correct constraint: (or equality for the budget line).

1 mark: Correctly defines as prices and as quantities.

1 mark: Correctly defines as income/budget.

(b) 3 marks:

1 mark: Explains that the constraint determines the feasible/affordable set of bundles.

1 mark: Explains that rational choice implies choosing the most preferred bundle within that feasible set.

1 mark: Explains trade-off/opportunity cost idea: more of one good requires less of the other due to limited income and given prices.

FAQ

Rational choice can be modelled with limited information: consumers optimise based on the information they have (or believe).

Common approaches include:

Using expected outcomes (e.g., expected value)

Treating search as costly, so consumers stop searching when expected gains are small

Assuming simple rules of thumb that still respect constraints

A constraint is binding when it actually restricts the chosen option.

If the budget constraint is binding, the chosen bundle lies on the budget line (spending all $I$).

If it is not binding, the consumer would have unspent income at the chosen bundle (possible when other constraints dominate).

Yes. Rationality is about consistency with an objective, not the objective itself.

Objectives could include:

Meeting a nutrition target at minimum cost

Avoiding risk

Following ethical or environmental rules

The key is that the chosen option is the best feasible one relative to that goal.

They change the effective price paid by consumers and therefore reshape the budget set.

For example:

A per-unit tax increases the consumer’s effective price, shrinking affordability of that good.

A subsidy lowers the effective price, expanding affordability.

These policies alter feasible bundles even if money income $I$ is unchanged.

Time is scarce and must be allocated across activities, so it creates a feasibility boundary.

A time-budget approach:

Assigns each activity a time requirement

Limits total time to available hours

Treats “full cost” as money plus time cost (often valued using an hourly wage or opportunity cost)